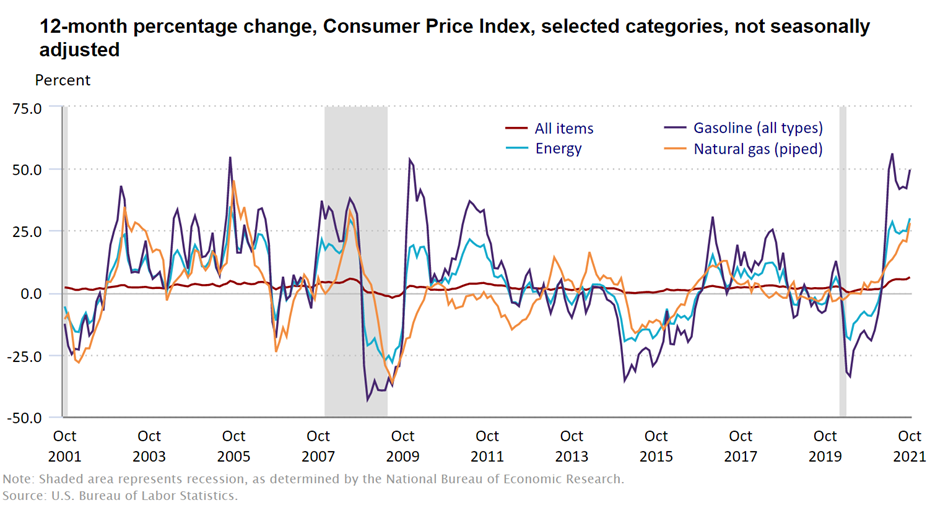

I look at a lot of charts, so you don’t have to. But here’s one I need to share. It’s a partial breakdown of product prices by the U.S. Bureau of Labor Statistics, that’s the group of wonks who tell us (formally) what inflation is doing. Check out the more recent data on the far right. I’ve peeled out the various energy-related trends so you can see just out of control they’ve gotten of late.

Not nerdy enough for you? You can mix and match your own factors here. #DataIsCool

Current supply chain woes aren’t just about goods getting to Southern California, or how efficiently Southern Californian dockworkers can get those goods in I’ve got two bits of good news and one bit of bad news.

Good1: The good news is that as high as energy prices have recently become in the United States, relief is on the way. Oil and natural gas prices have now been high enough for long enough that America’s shale operators have steadily expanded operations and fresh production is already feeding into the system. We might not feel that relief in the form of lower prices until March, but relief is still on the way.

Good2: As bad as prices seem, it is way worse everywhere else. Natural gas prices in Europe are now ten times what they are in the United States, and the Europeans have zero reasons to expect their situation to improve one whit this year. Or next year. Or the year after. Europe has next to no local oil or natural gas production, and no shale sector to speak of. Instead, the Europeans have chosen to rely on solar and wind power (on the world’s cloudiest and calmest continent, no less), with a bit of bridge assistance from…the Kremlin.

Bad1: Good1 might make you exclaim a sigh of relief. Whew! This too shall pass. Weeeeell, not really. Just because I don’t see energy inflation holding up in the United States does not mean that I don’t see us entering one of the weirdest periods of economic transition in American history. You name the sector — finance, manufacturing, housing, agriculture, transport, commodities — we are in for at least the strongest inflation we’ve seen in this country since the 1970s.

Breaking down that is going to require a great deal more than a newsletter.

Join us for the final installment of our series on the future of the global and American economies in an age of deglobalization.

REGISTER FOR PART III: THE FACE OF INFLATION

Part II: Supply Chains No More

Join us Friday, November 19th at 1p Eastern for our webinar about the challenges facing global supply chains: