Gazprom, the Russian state’s gas monopoly notified its European customers that it was declaring force majeure in its supply contracts going back to June 14, citing “extraordinary circumstances” preventing the delivery of natural gas. It’s easy to guess what the circumstances referenced are–the conflict in Ukraine, sanctions, etc. Is this just Russian brinksmanship? A negotiating chip?

Maybe. Probably not. We shouldn’t forget that Nord Stream 1, the direct gas pipeline between Russia and Germany, is currently undergoing routine maintenance until later this week. There’s still no strong indication that Russian gas supplies will resume in whole or in part, and with today’s declaration Moscow has legal cover to halt energy supplies to the economic heart of Europe. As if legal cover is all Russia needs.

In the links below, we’ve included a series of videos I’ve recorded over the past few months that outline Russia’s strategy, Europe’s rather pitiful few options, and the rather bleak reality that Russia increasingly sees itself not just at war with Ukraine, but in direct conflict with Europe. To expect energy supplies to continue as normal is a fantasy that not even the most optimistic German industrialists can pretend to believe in anymore. The EU–especially Germany–and Russia both saw the increase of energy interconnectivity and pipeline politics (or “diplomacy”) or the past few decades as a game of increasing leverage. The question was always, for whom? Europe always hoped that it could entice Russian good behavior through economic linkages and purchase contracts. We’re likely to see in coming days where the power in this relationship, pun intended, really flows from.

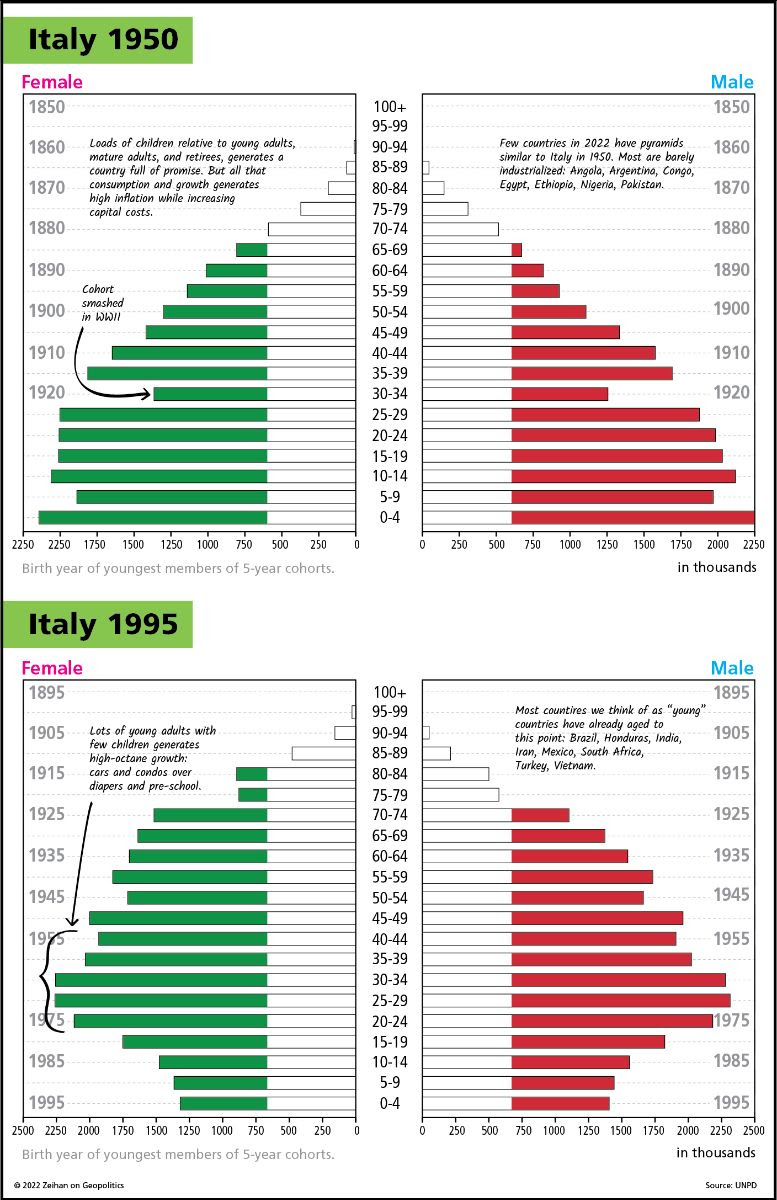

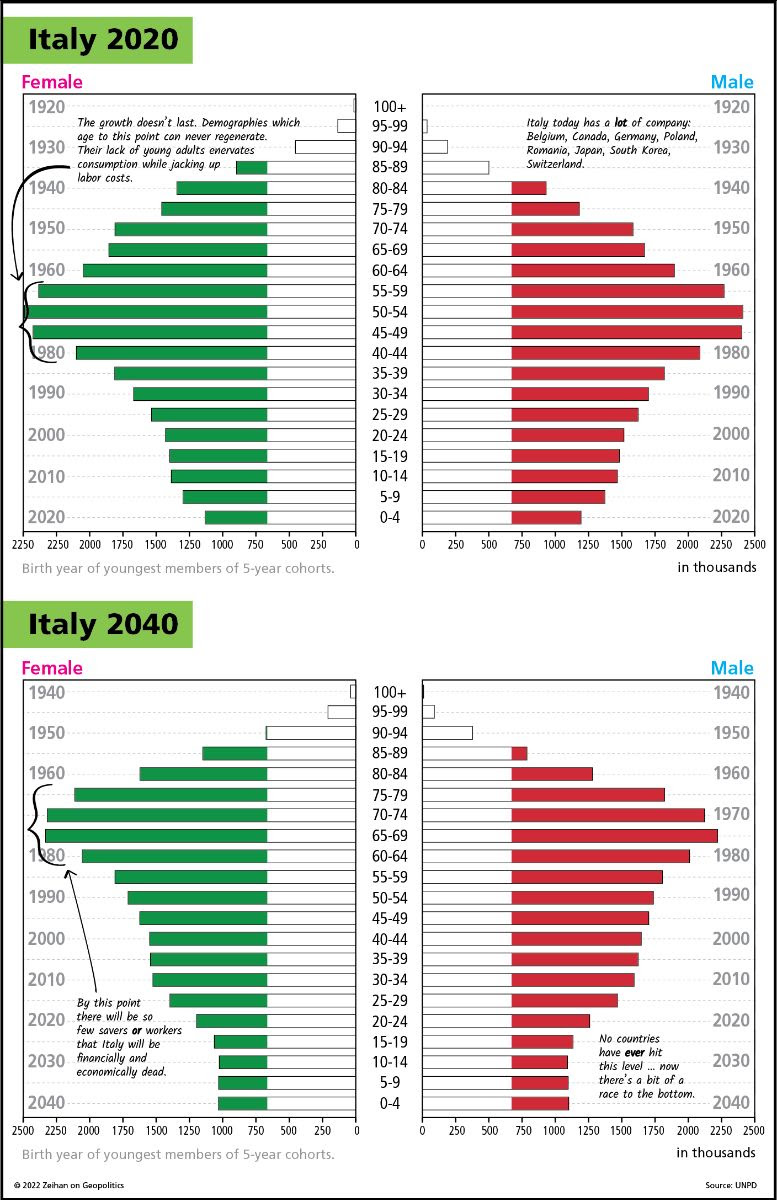

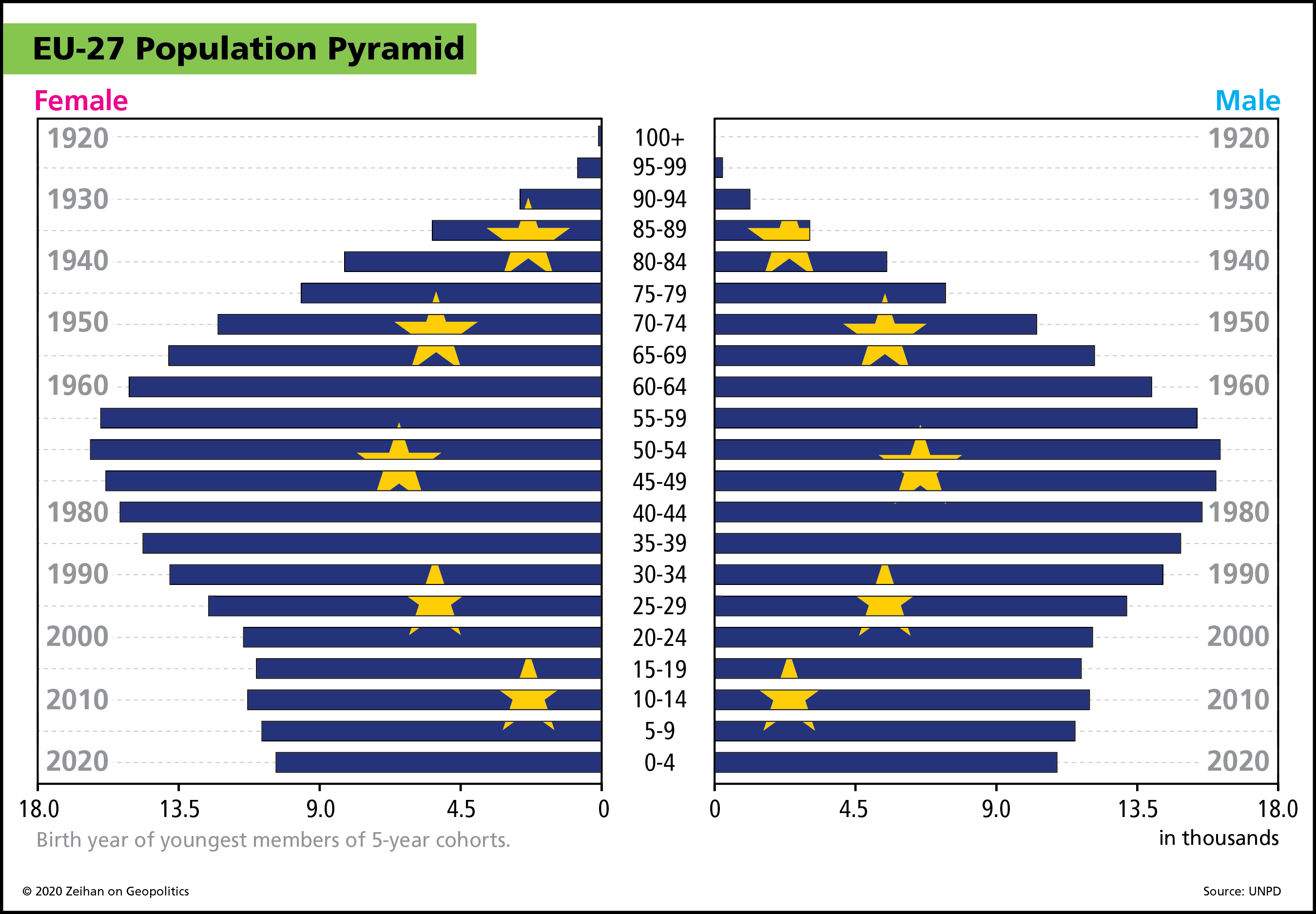

What we have here are two population pyramids, telling two very different stories of ostensibly the same country. The data is arranged numerically by sex, with simple mortality causing the numbers to shape up like a pyramid. At least, the chart looks like a pyramid in societies with a high enough fertility rate to offset deaths due to old age.

Take a look (and a read). Italy is most assuredly not alone in its rapid demographic decay.

Here at Zeihan On Geopolitics we select a single charity to sponsor. We have two criteria:

First, we look across the world and use our skill sets to identify where the needs are most acute. Second, we look for an institution with preexisting networks for both materials gathering and aid distribution. That way we know every cent of our donation is not simply going directly to where help is needed most, but our donations serve as a force multiplier for a system already in existence. Then we give what we can.

Today, our chosen charity is a group called Medshare, which provides emergency medical services to communities in need, with a very heavy emphasis on locations facing acute crises. Medshare operates right in the thick of it. Until future notice, every cent we earn from every book we sell in every format through every retailer is going to Medshare’s Ukraine fund.

And then there’s you.

Our newsletters and videologues are not only free, they will always be free. We also will never share your contact information with anyone. All we ask is that if you find one of our releases in any way useful, that you make a donation to Medshare. Over one third of Ukraine’s pre-war population has either been forced from their homes, kidnapped and shipped to Russia, or is trying to survive in occupied lands. This is our way to help who we can. Please, join us.

I decided to limit my harassment of everyone (and my staff) this past holiday weekend, but I did want to thank everyone for being so supportive of the new book, The End of the World Is Just the Beginning. It is doing disturbingly well on the charts and maybe, just maybe, we’re looking at a bestseller here? We’ll know when the lists come out June 26.

Anywhatever, the world didn’t stop simply because Americans were celebrating their newest national holiday and I was engaging in some much needed decompression, so I’ve taken the liberty of putting together a much-longer-than-normal videologue to encapsulate the two big events over the weekend. Both are Ukraine War related.

The first deals with a new flash point in the conflict. Not in Ukraine proper, but instead directly between the Europeans and Russians over Russia’s Baltic enclave of Kaliningrad. The second deals with the early stages of the collapse of the European energy system, with the immediate event being Germany’s decision to move back to coal in a very big way.

War. Energy shortages. Transport breakdowns. Famine on the horizon. It’s getting real out there. Stay safe.

Here at Zeihan On Geopolitics we select a single charity to sponsor. We have two criteria:

First, we look across the world and use our skill sets to identify where the needs are most acute. Second, we look for an institution with preexisting networks for both materials gathering and aid distribution. That way we know every cent of our donation is not simply going directly to where help is needed most, but our donations serve as a force multiplier for a system already in existence. Then we give what we can.

Today, our chosen charity is a group called Medshare, which provides emergency medical services to communities in need, with a very heavy emphasis on locations facing acute crises. Medshare operates right in the thick of it. Until future notice, every cent we earn from every book we sell in every format through every retailer is going to Medshare’s Ukraine fund.

And then there’s you.

Our newsletters and videologues are not only free, they will always be free. We also will never share your contact information with anyone. All we ask is that if you find one of our releases in any way useful, that you make a donation to Medshare. Over one third of Ukraine’s pre-war population has either been forced from their homes, kidnapped and shipped to Russia, or is trying to survive in occupied lands. This is our way to help who we can. Please, join us.

I’m re-sharing a couple of videos from early May to highlight a couple key trends coming to a head: the EU ban on Russian oil imports, and a continuing challenge of indemnification for ships carrying cargoes of Russian goods–oil, stolen Ukrainian grain, etc.

On the first, it’s taken Europeans months to hammer out an agreement and a timeline–with plenty of caveats–but replacing your largest oil supplier overnight is a considerable feat. But EU leaders came out over the weekend announcing that a general framework had been reached, seeing most of the EU taper off of Russian oil by year’s end. One of the biggest exemptions is Russian crude delivered by pipeline, a necessary boon for landlocked importers like Hungary, and how Russia delivers a third of its oil to Europe.

While it’s easy to be cynical, we should not gloss over the fact that over the next several months the world’s largest economic bloc will be scaling down nearly 70% of its primary fuel source. Moscow is already adding European nations to its “do not sell list,” with the Netherlands joining Finland, Bulgaria and Poland in having to seek workarounds in accessing piped Russian natural gas deliveries. The Dutch have one of Europe’s largest LNG import terminals, and there is a lot of interconnected gas infrastructure to keep supplies moving around in the meantime, but the writing is on the wall.

For now.

The EU’s largest customers of Russian energy, Germany and Turkey, will the be ones to watch here. German corporations and labor unions remain opposed to a full German embargo of Russian natural gas and the Turks… well, when it comes to NATO and EU directives and sanctions packages, the Turks are going to do what’s best for Turkey.

Which makes the increasingly difficult time Russian cargoes are having all the more interesting. Private insurance companies, crews, captains, and port workers are simply refusing to cover, load, unload, and give harbor to Russian ships and Russian goods. While the EU is putting together another (the sixth!) sanctions package that will touch on some of these issues, the global shipping industry has shown a remarkable willingness to self-police and oppose Russian participation in regional and global shipping markets. China and India may continue to buy Russian crude (for now), but they’re doing so with state-owned ships and with state-backed insurers underwriting everything. Both economies are far too large to handle all of their goods trade in such a matter, however, and it will be interesting to see if their purchases of heavily-discounted Russian crude oil will be met with any market-driven consequences from the shipping industry.

Here at Zeihan On Geopolitics we select a single charity to sponsor. We have two criteria:

First, we look across the world and use our skill sets to identify where the needs are most acute. Second, we look for an institution with preexisting networks for both materials gathering and aid distribution. That way we know every cent of our donation is not simply going directly to where help is needed most, but our donations serve as a force multiplier for a system already in existence. Then we give what we can.

Today, our chosen charity is a group called Medshare, which provides emergency medical services to communities in need, with a very heavy emphasis on locations facing acute crises. Medshare operates right in the thick of it. Until future notice, every cent we earn from every book we sell in every format through every retailer is going to Medshare’s Ukraine fund.

And then there’s you.

Our newsletters and videologues are not only free, they will always be free. We also will never share your contact information with anyone. All we ask is that if you find one of our releases in any way useful, that you make a donation to Medshare. Over one third of Ukraine’s pre-war population has either been forced from their homes, kidnapped and shipped to Russia, or is trying to survive in occupied lands. This is our way to help who we can. Please, join us.

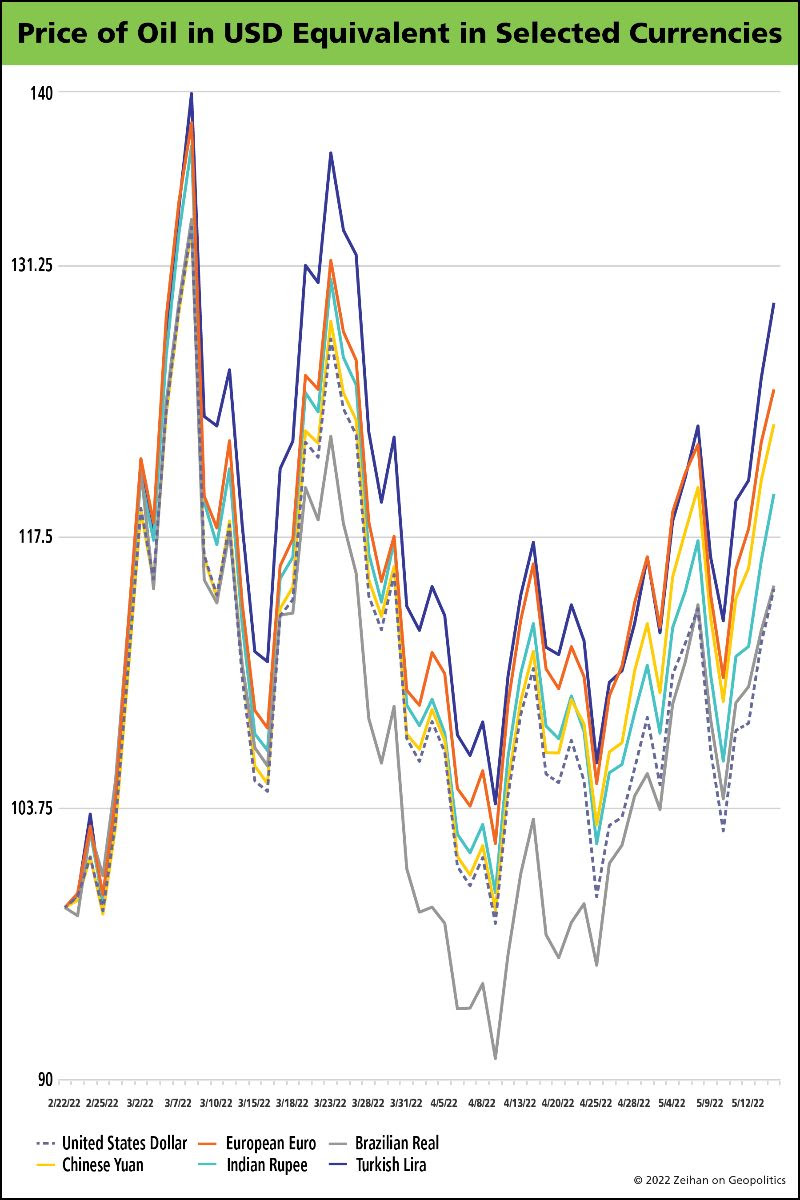

In the worlds of finance, trade, economies, currencies and energy there is a lot going on. We’ve a war in Ukraine that will likely generate the largest oil dislocation in modern history. The global Baby Boomer generation is retiring and taking their money with them, generating the largest financial dislocation in modern history. Presidents Trump and Biden are following the same script on trade issues, generating the largest trade dislocation in modern history. And the Federal Reserve is tightening monetary policy in an effort to tamp down inflation.

The implications of all these seismic shifts are many and massive. Here’s two of them:

Whenever countries are struck by economic shocks – like, say, now – investors look for safer places to stash their money. Less money into tech, more into consumer products. Less money into Brazil, more into Europe. The safest of all safes is the United States, and so the U.S. dollar is on a bit of a tear, rising by roughly 10 percent verses most of the world’s currencies since the beginning of the year.

A rising dollar has any number of outcomes, but the one making the biggest splash at the moment is its impact upon energy markets.

Oil prices were already rising due to a variety of factors ranging from insufficient investment in new projects over the past several years, to disruptions in trade patterns, to, of course, the Ukraine War. For the United States this is known and obvious. But all commodity trade is denominated in U.S. dollars. Oil is no exception. Combine oil’s price rise with a strengthening dollar and much of the world takes a double hit.

Brazil’s real has largely kept pace with the U.S. dollar, so this energy hit doesn’t land on Brazilians quite as hard. But Europe and Turkey? Those locales heavily depend upon Russian crude. Not only does that challenge their supply systems, it’s also contributed to the pair’s suffering from significant currency weakness. The end impact? In local currency terms, internationally sourced oil now costs 10-15% more in Europe and Turkey than it does in the United States.

Unfortunately, there is little reason to expect the world’s energy situation to improve within the next half decade, nor is there reason to expect the U.S. dollar to go anywhere but up for years to come. But that is a story for another day.

That day is … June 8. That’s when we’ll be hosting our next seminar, Inflation: Navigating the New Normal. You can sign up here.

Here at Zeihan On Geopolitics we select a single charity to sponsor. We have two criteria:

First, we look across the world and use our skill sets to identify where the needs are most acute. Second, we look for an institution with preexisting networks for both materials gathering and aid distribution. That way we know every cent of our donation is not simply going directly to where help is needed most, but our donations serve as a force multiplier for a system already in existence. Then we give what we can.

Today, our chosen charity is a group called Medshare, which provides emergency medical services to communities in need, with a very heavy emphasis on locations facing acute crises. Medshare operates right in the thick of it. Until future notice, every cent we earn from every book we sell in every format through every retailer is going to Medshare’s Ukraine fund.

And then there’s you.

Our newsletters and videologues are not only free, they will always be free. We also will never share your contact information with anyone. All we ask is that if you find one of our releases in any way useful, that you make a donation to Medshare. Over one third of Ukraine’s pre-war population has either been forced from their homes, kidnapped and shipped to Russia, or is trying to survive in occupied lands. This is our way to help who we can. Please, join us.

Russia and Europe are tilting toward confrontation. The European defense posture for the past 70+ years has been predicated on NATO–a fancy acronym for “the United States is our security guarantor.” What can Europe expect following the US presidential election in November?

If you enjoy our free newsletters, the team at Zeihan on Geopolitics asks you to consider donating to Feeding America.

The economic lockdowns in the wake of COVID-19 left many without jobs and additional tens of millions of people, including children, without reliable food. Feeding America works with food manufacturers and suppliers to provide meals for those in need and provides direct support to America’s food banks.

Food pantries are facing declining donations from grocery stores with stretched supply chains. At the same time, they are doing what they can to quickly scale their operations to meet demand. But they need donations – they need cash – to do so now.

Feeding America is a great way to help in difficult times.

The team at Zeihan on Geopolitics thanks you and hopes you continue to enjoy our work.

There is no such thing as “Europe.” Yes, there’s this political-economic grouping called the EU, but two of Europe’s most important countries are not members. Yes, there’s this political-military grouping called NATO, but it is functionally run from a different hemisphere. Recent developments might – emphasis on might – change this, but the Europeans aren’t there yet.

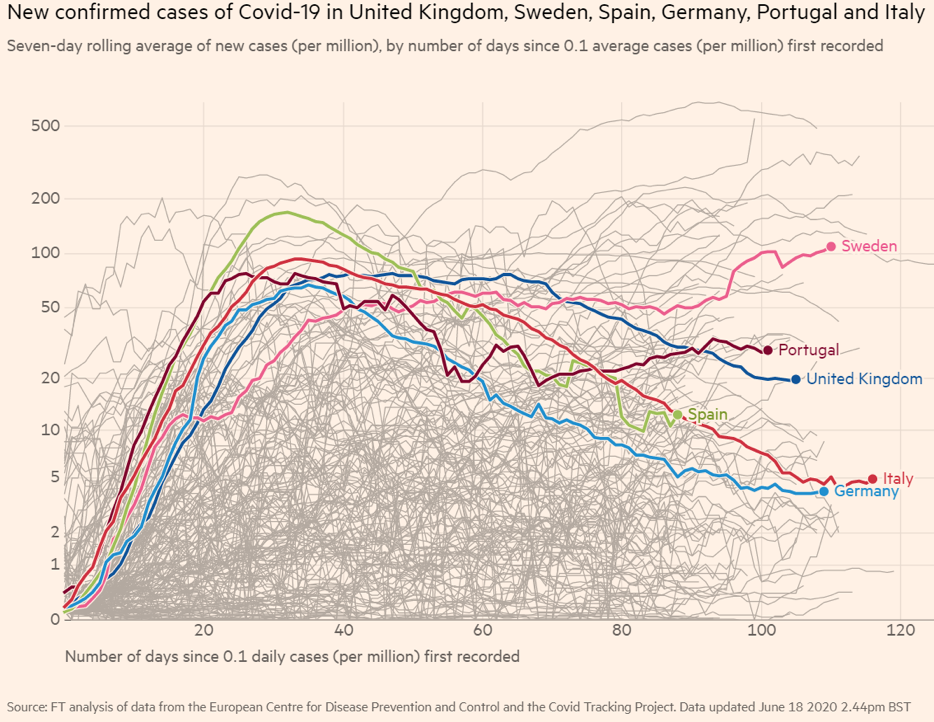

With over 30 different political and decision-making systems, there is plenty of room to find fault with any broad assessment. But as regards the ongoing coronavirus pandemic, the fact remains that overall, Europe has been moving in the direction of fewer and fewer cases.

(Many, many thanks to the Financial Times for providing the data interface that makes this graphic possible. You can visualize your own data pulls here.)

The early phases of the epidemic were harsh in many places. In large part, it was because the Europeans had, at best incomplete information from which to base their policies. For the Italians and Spanish who suffered through coronavirus’ initial assault, they were simply caught off-guard. The result? Much of Europe enacted lockdowns whose intensity and airtight nature was only surpassed by the 1984-style lockdowns in Wuhan. (In Paris, you had to apply for a government permit to leave your home to shop for food. The permit only lasted for one hour.)

There’s also the issue of vectors. The suspected patient zero in Italy was initially misdiagnosed and so went from the hospital almost directly to a massive soccer game, becoming Europe’s first superspreader. Most people came to and left the game via bus, enabling the virus to spread liberally. A few of those buses went to Spain, which is why Spain became the second hardest-hit country in Europe.

In contrast, Austria and Germany’s superspreaders were a bunch of 20-somethings at ski parties in the Alps. The Austrians and Germans not only had a bit more warning than the Italians and Spaniards, but their epidemics were also among young millennials – a group that COVID doesn’t impact that harshly. The Austrians and Germans locked down their elderly populations, ran a rigorous testing and tracing program, and more or less nipped the problem in the bud.

Of course, despite caseloads moving in the right direction overall, this is not over. The variation of Europe’s COVID policies to date will also define the epidemic’s future:

Germany is playing it safe and has retained its de facto ban on all extra-European travelers until at least August 31st. Considering caseloads in the Western Hemisphere and the Middle East show no signs of dropping, expect this date to get pushed back.

In contrast, consider Portugal. Portugal is one of the many European countries suffering from a terminal demography; its birth rate crashed back in the late 1970s, never recovering, and the Portuguese economy is now a moribund mess. Since Portugal lacks the industrial base of a country like Germany, Portugal’s only growth sector is tourism. COVID killed tourism. Portugal recently released all restrictions in a desperate attempt to forestall what threatens to be an unending economic depression…which means Portugal is one of only three EU countries where caseloads are increasing.

Nor did everyone in Europe follow even remotely similar lockdown protocols. As mentioned earlier, the Europeans were working with incomplete information as the pandemic started, and not everyone came to the same conclusions. The British and Swedes balked at the economic damage full lockdowns would cause, and reasonably believed any effective vaccine would not be available for years. Add in that coronavirus has the highest infection rate of any public health threat since measles and a fairly low mortality rate, and both governments felt containment was a fools’ errand. They opted for management. Both decided to pursue herd immunity in an attempt to build a firewall against the virus within their populations.

Britain ultimately blinked, largely due to the carnage being wrecked in Italy which suggested much higher death counts than initially suspected. The Brits belatedly followed a more traditional lockdown approach. The delay landed the Brits with one of Europe’s highest infection rates as well as a lengthy plateau. It was only in mid-May that the Brits finally got COVID cases bending downward. The Swedes, on the other hand, stuck with the plan. Sweden now faces infection rates among the world’s highest, recently surpassing even the United States.

The real tragedy in Sweden was that knowing what we all knew back in April, the herd immunity strategy wasn’t silly, but instead a calculated risk. The Swedes assumed a functional vaccine would remain unavailable for years, and so concluded that building immunity within the population was the only sustainable route forward. Now it appears a functional vaccine will be available before the end of 2020, with mass distribution beginning (although not being completed) in 2021. The facts as we understand them have changed. Sweden’s sacrifice may have been for nothing.

If you enjoy our free newsletters, the team at Zeihan on Geopolitics asks you to consider donating to Feeding America.

The economic lockdowns in the wake of COVID-19 left many without jobs and additional tens of millions of people, including children, without reliable food. Feeding America works with food manufacturers and suppliers to provide meals for those in need and provides direct support to America’s food banks.

Food pantries are facing declining donations from grocery stores with stretched supply chains. At the same time, they are doing what they can to quickly scale their operations to meet demand. But they need donations – they need cash – to do so now.

Feeding America is a great way to help in difficult times.

The team at Zeihan on Geopolitics thanks you and hopes you continue to enjoy our work.

The past few several weeks have been busy for the Europeans, easily generating more events of consequence than at any time since at least the 2007 financial crisis. There is no specific trigger event here that makes much sense without absorbing the context first, so I’m just going to do what I do and start at the beginning.

Germans aren’t normal.

I don’t mean that as a condemnation of their weather or dourness or food or their linguistic tendency to link a dozen or more words together into typographical nightmares, but instead that Germany’s peculiar geography has made the Germans somewhat…peculiar.

Germany’s geography is the best and worst of all worlds. Best in that it boasts four major and a dozen minor rivers as well as ample stretches of flat land to both ease internal transport and make for cheap development. Worst in that Germany’s most rugged terrain is in the country’s interior while its flattest lands are on its borders, making it easier (historically speaking) for most Germans to integrate with their (non-German) neighbors rather than their own co-ethnics.

Historically, this has made German lands among the most bloodsoaked in Europe, with the whole area being preyed upon over and over and over. The first “Germany” was Charlemagne’s, and it only lasted so long as the great monarch was alive. The Holy Roman Empire was a primarily German entity (occasionally referred to as the First Reich), but it wasn’t even remotely united, comprised as it was by sometimes over 1000 (often mutually warring) statelets.

It was only with the onset of industrialization in the 1800s that Germans were able to use rail and electricity to overcome their internal geographic complexity and achieve unity. But unity doesn’t automatically translate into happy-fun-play-time. The second and third Reichs were Germany’s Imperial and Nazi incarnations. Those governments’ attempts to impose writs on the wider European neighborhood resulted in the most catastrophic wars humanity has ever experienced. For the following 45 years, Germany was the very definition of not united – split into two pieces to serve as mutually-opposing frontline states in the Cold War.

In the years since the Berlin Wall fell, the newly-united Germany – or Fourth Reich if you prefer – has been taking a wonderous vacation from history. It doesn’t need to fight to remain unified; America’s imposition of a global Order makes that unnecessary. It doesn’t need to protect its borders; American-dominated NATO takes care of security issues. It doesn’t need to fight for access to either raw materials or consumer markets. The Americans’ global structure has enabled the rise of the European Union within Europe, and has allowed German firms access to a worldful of consumption. All Germany needs to do to be Germany today is…be. And so the Germany of today is united, free and at peace…without the Germans needing to do a damn thing.

For those of you who would like Germany to exercise more decisionmaking power and take security matters into its own hands, I refer you to literally any book on European history between 1848 and 1945 to highlight why that might not be the fabulous idea you assume it to be.

Anywho, there are now three intersecting problems that all independently threaten Germany’s blissful existence.

First, the Americans are done holding up the collective civilizational ceiling of the world. The United States created the global Order to fight the Cold War, and that war ended when the Berlin Wall fell. The Americans have been edging away from, well, everything, ever since. The day of final abandonment was always going to come, it is now here, and everyone who used to shelter under the American security umbrella or benefit from a globalized economy must figure out a new way forward. That applies to Germany as much as everyone else.

Second, the German economic model of mass exports is running out of road. Mass exports requires a large, highly-skilled workforce heavy with people in their late-40s through early-60s. Germany has had that for the past 15 years, but those skilled workers collectively are crossing the retirement threshold this decade. With no replacement generation coming up through the ranks, Germany can neither consume what it produces today, nor maintain its current production for much longer. That eliminates both the basis of the German economy and the German tax base. Something new, something radical, something that utilizes resources beyond Germany, is required.

Third, the EU – the only meaningful piece of the Order the Americans do not directly control and so the only possible anchor the Germans have keeping them in a safe, peaceful, united Europe – is in mortal danger. In part it is because much of Europe faces the same security and export dependence upon the Americans as the Germans do. But there’s another problem.

Geography.

Northern Europe is flat and well-rivered and so countries there can achieve efficiencies and economies of scale. Southern Europe is rugged and lacks rivers and so cannot. Exceptions abound in a continent as varied as Europe, but the bottom line is that Southern Europe will never be able to compete with Northern Europe economically, just as Northern Europe cannot hope to compete with Southern Europe when it comes to sun, fun, food and flair. (France has a foot in both worlds which is part of what makes the French…well…French.) Anywho, the bottom line is that there is no European Union without both parts of Europe, so the question becomes how to keep it all stitched together without either the American-led Order or the ability to access markets from far beyond Europe?

There is no good answer. Even more problematic, what might prove a good answer for Ireland would be hilariously inappropriate for Croatia. What most everyone can agree on, however, is that Europe as a combined entity will be better able to get what it needs than the EU’s constituent members acting independently. And so Europe has been limping along since the 2007-2009 financial crisis, economically suppressed, strategically adrift, politically riven…but with no one (save the Brits) willing to pull the plug on the whole project.

In my new book, Disunited Nations, I’ve got a whole chapter on called “Superpower, Backfired” on the hows and whys Germany ended up in this situation and where it is likely to lead.

And then there’s the coronavirus.

Just as there are differences in European financial and economic structures on a country-by-country basis, so has the virus impacted EU members differently.

It comes down to vectors and weather. Most of the cases in Germany originated at a series of Alpine ski parties for 20-somethings. When the virus started to spread, it spread among the population most able to survive it. In addition, late-winter and early-spring in Germany isn’t exactly tourist season, so most elderly stayed locked up at home. Germany was able to address the virus outbreak relatively quickly and move on.

Not so in Italy. Patient zero went to a massive outdoor soccer game and became one of the first COVID superspreaders. Elderly Italians are also more likely to live in a multi-generational household than elderly Germans because…well… sun, fun, food and flair. It wasn’t long before the Italian health care system was overwhelmed.

Finances matter too of course. Germany has been whittling away at its national debt for twenty years, and so had plenty of dry powder to apply to the crisis without needing to ask anyone for help. Italy…hasn’t. When the crisis exploded upon the Italians they almost instantly ran out of cash and had to turn to the EU hat-in-hand for help.

The response was underwhelming. The Germans – backed up by the European Central Bank (ECB) chief – told the Italians that saving Italy wasn’t their job. As a point of comparison, across the Pond the Americans slapped together humanity’s largest-ever stimulus program in a matter of days.

It didn’t take long for German Chancellor Angela Merkel to realize that the situation was untenable. It wasn’t so much that Italy and others were facing fiscal collapse because of COVID (although they were), it was that Merkel knows full well that the road the EU is on means that Italy and others would inevitably face fiscal collapse. COVID just brought the end forward by a few years. The question Europe has been struggling with since 2007 – now that we are certain this is unsustainable, what do we do? – had moved from the hazy future to the here-and-now. And Merkel simply didn’t have an answer. If she had, she would have produced it. Years ago. And so the demurring and dithering continued.

Ironically, it took events within Germany itself to force the issue. On May 5 the German Constitutional Court ruled that methods the ECB were using to keep some of Europe’s weaker states on life support were unconstitutional. Specifically, the ECB can only purchase government debt if it does so proportionally to the size of all eurozone economies. Since the Germans have been paying their debt down, there wasn’t much German debt left to buy. And since the Italians were in a COVID pickle, the Italians needed to issue more debt. The ECB did the logical thing and put its resources where they were needed. The German court ruled that the ECB’s logic violated European law in general and the German constitution in specific, and that the German government must cease all cooperation on the issue within 90 days.

Running the European Central Bank without the participation of Europe’s largest economy would open up a hilariously huge barrel of worm-ridden monkeys, taking us down paths so convoluted and impractical as to be positively Venezuelan. But those monkeys and paths all take us to the same place: no European bond market, no European currency, and – very likely – no EU.

A world without America. A Europe without the EU. Germany left to look after its economic and security issues on its own, likely in competition with its current EU partners. That is nothing less than Merkel’s worst-case scenario, and so she did the only thing she felt she could:

On May 20 in a joint presser with French President Emmanuel Macron, Merkel proposed the EU’s first mutualized debt. For those of you not in finance, that’s a fancy way of saying that not only will Germany co-sign for some Italian borrowing, but that Berlin will agree up front to use the EU’s common budget to pay for some Italian spending. Simply put, Merkel committed Germany to paying for the ongoing existence of the EU in general and the EU’s weaker members in specific in the hopes of buying more time to find a better solution.

Many many details remain.

How big of a fund are we talking about? At present the combined floats of the Germans, French and the EU Commission total something around 1.5 trillion euro. (Right now that’s about $1.65 trillion US, so, you know, real money.) That’s roughly ten times the current total EU budget. That would probably cover the EU’s current needs this year, but only this year. And all the proposals to date are nothing more than one-offs designed to counter COVID impacts. This doesn’t actually help the EU survive in the long-run. For this to work and for the EU to function as a true superstate, the EU needs a full transfer union of at least these volumes annually.

Who would get the funds, and who would pay the funds back and how? At present the idea is to funnel everything through the European Commission, with funds being dispersed into (suddenly engorged) EU programs, while payback would come from the various member states who fund the Commission directly. Needless to say, that would be wildly inefficient and cumbersome, although it would wildly strengthen the EU’s administrative core and take Europe a few big steps down the road to full federalization on the American model.

Can this – institutionally – happen? It doesn’t look great. Big things like this normally require a treaty, and the EU has rarely managed negotiating and ratifying a treaty on anything less than a decade timescale. Moving forward without a treaty would still require unanimity, and several EU states have already voiced their vociferous opposite to the plan.

But, again, let me be clear here. Between the Americans’ withdrawal and Europe’s demographic implosion, the very existence of the European Union is at stake. This was always true. This was always inevitable. But COVID and the German court ruling makes the crisis imminent. In a Europe without either America or the EU, Germany must reorganize into a form that enables it to protect and further its own interests without outside support. This isn’t “simply” an existential crisis for the Germans. It is an existential crisis for all Europeans.

And historical annihilation tends to focus the mind.

So let’s take a brief look at the four hard-nos in this debate: Austria, the Netherlands, Denmark and Sweden.

The bulk of Austria’s population lives on the southern watershed of the Danube. The entirety of the Netherlands lies atop the delta of the Rhine. Those two rivers are core Germany population, industrial and transport zones. The Austrians and Dutch have zero geographic insulation from Germany.

Neither country may like the financial implications of where the debt-mutualization path leads, but both are deeply, painfully aware of precisely where European collapse leads: a Germany forced or induced to seek out German national interests to the detriment of its neighbors. Historically speaking, once the Germans get rolling, maintaining an independent Austria or Netherlands is pretty much impossible. The Austrians and the Dutch know this. Both can be armtwisted into accepting Merkel’s (costly) logic.

And that assumes Merkel doesn’t do her traditional thing. Unlike most leaders, Merkel tries to shun the spotlight and instead lead from behind. She allows her opponents to stake out bold positions, and then unobtrusively steps back from the shouting and quietly cobbles together a majority position that doesn’t include the troublemakers, leaving them with the option of joining the crowd or screaming into the void. She’s done this (repeatedly) to consolidate control of her political party in Germany. She’s done this (repeatedly) to defang troublesome governing coalition partners. She’s done this (repeatedly) to guide Europe through the financial crisis. It is highly likely that the Austrians and Dutch will be Merkel’s next void-screamers.

Denmark and Sweden are a different sort of challenge. Sweden doesn’t border Germany, while the bulk of the Danish population lives not in peninsular Denmark, but instead on the island of Zealand. Culturally, economically, and above all strategically both only have one foot in Continental Europe. In particular, both have historically been closer to the United Kingdom (and dare I say, the United States) on defense issues than to Germany. As such neither are even members of the eurozone. That makes the pair less likely to be cajoled into participation, but it also means there is another potential path.

Rather than run the funds and the debt through the EU budget, the funds could be kept aside as a purely eurozone project which could exempt any EU state that didn’t also use the European currency. (In addition to Denmark and Sweden, this list also includes a variety of Central European states such as Poland, Hungary and Romania.) It’d be messy organizationally, and arguably unnecessarily so, but the EU does tend to excel at spawning unnecessarily messy organizational structures.

Anywho, lots of details to work out. What Merkel and Macron are attempting on the fly is the first real step towards federalizing the European Union. Europe has a common currency (which not everyone is a part of) and a common foreign policy (which requires unanimity) and a common market (regulated by national governments), but until it has a common budget it is most certainly not a superstate and it is most certainly not pooling its national resources into a more powerful, more cohesive whole.

That more powerful, more cohesive whole is the only thing that matters if the EU is to persist through contorting geopolitical and demographic circumstances. There is no guarantee the current plan will be adopted, much less work, much less expand into something that would make the EU a true, durable power. But the fact remains that for the first time in years I have a faint glimmer of hope that this thing we call the European Union might, just might, survive.

On June 3 Melissa Taylor and Peter Zeihan will be hosting a video-conference on Manufacturing in a New Era. We’ll address the future of automotive, automation, reshoring, COVID’s shattering of supply chains, consumption shifts, as well as get you an update on the deepening trade war.

For those of you who don’t want to pop for the fee, we’ve recently completed a video on our projected shape of the COVID epidemic to come. You can watch it for free here.

Our June 3 manufacturing video-conference is only the first of a series which will include events focusing on Mexico, China, Energy and Agriculture. Scheduling and sign up information can be found here.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

The British government announced March 27 that Prime Minister Boris Johnson tested positive for coronavirus, making him the first world leader to do so. As the United Kingdom is an advanced democracy, here at ZoG we are not overly concerned with Johnson’s isolation and perhaps incapacitation or even death. Part and parcel of democracies is that succession is part of life. The UK will get through this one way or another.

However, there are many countries that are not democracies and there are many world leaders far older than Johnson…

In the age of coronavirus, Europe’s near-term future is bleak.

European headlines in coming weeks will be about coronavirus deaths. In large part the issue is demographic. Coronavirus is far more likely to kill those over aged 60. The average European is approximately a half-decade older than the average American. Only the Japanese are older.

Specifically, Italy hosts the world’s second-oldest population, while Germany ranks 5th. Meanwhile, many of the “new” European countries in Central Europe are not all that much younger, while also lacking German- or Italian-quality health care. Others, Ireland, Greece and Spain come to mind, have had to deal with financial crisis by cutting services. Services like health care. The United Kingdom, courtesy of the dual forces of Brexit and coronavirus, are seeing many health care professionals who are not UK citizens but who were able to work in the UK during the Kingdom’s EU membership, fleeing back to their home countries at the worst possible time.

The demographic issue will hurt Europeans on more than simply mortality figures.

People under 45 tend to be a society’s big spenders. They buy cars and homes. They go to university. Such consumption is what drives most modern economies. But not in Europe. Europe’s young cadre is thin and getting thinner by the year. Most European countries – Italy and Germany most notably – have already aged to the point that any sort of demographic rebound is now impossible. They simply don’t have enough people who could even theoretically have children. There certainly aren’t enough people of the right age demographic to drive a consumption-driven rebound.

Which makes mitigating the economic damage of coronavirus structurally impossible. The sort of consumer stimulus which is the backbone of consumer-focused, anti-recession efforts in the United States simply wouldn’t work in Europe. On the whole, the European Union has aged into being little more than an export union. And in a time of global travel restrictions and virus-forced collapses in income and consumption, there just isn’t anyone to export to. All Europe can do is shelter in place, pray their health systems hold, and wait for the world to restart. So long as the coronavirus is impinging activity anywhere, a sustained European economic recovery is impossible.

But even if Europe had a favorable population structure, it lacks the institutional structure to hold the line against the virus anyway. It comes down to money.

Having its own currency enables the United States to print however much money it wants to risk, using that money to fund its own deficit spending. Neither W Bush nor Obama nor Trump would ever be confused with fiscal conservatives, but even now at the very beginning of the process we are seeing spending bloat unprecedented in American history – even at the height of World War II. By the second week of April, the Americans will have pumped over $2 trillion in financial relief into their system, or roughly 10% of GDP, in addition to monetary stimulus of a volume that stuns the imagination. The current spending wave has already seen the Federal Reserve hoover up over $1 trillion in securities, while the federal government is putting up to $1200 into the hands of the vast supermajority of American adults, with a $500 kicker for each child. Nor will this be the last such infusion. Expect another one sometime in the summer.

Europe lacks that sort of power and flexibility.

Part of the network of treaties that underpin the common European currency mandates not only fairly strict deficit ceilings (although those ceilings were suspended over the weekend) but far more importantly the Maastricht Treaty on Monetary Union took monetary responsibility out of member governments’ hands. European states can’t print currency. If they want to deficit spend, they have to raise the funds themselves. That takes time. That takes investors willing to put their money into governments’ hands.

Now technically, the European Central Bank can expand the money supply, and it will, but there are two problems. First, Europe never truly recovered from the 2008 financial crisis. Eurozone interest rates have been negative for years. What about unconventional measures? Much ballyhoo has been made in the United States about how the Federal Reserves purchased scads of bonds to prop up markets, purchases which peaked at just shy of 25% of GDP at the height of the financial crisis. The ECB’s balance sheet as of January 1, 2020, after a decade of calm and before coronavirus erupted, was twice that in relative size. It isn’t clear the ECB has much ammo to use here, conventional or unconventional.

Second, any ECB action raises the issue of whose bonds will the ECB buy? Will it be the country with the most likely chance of repayment (Germany), or the country facing the worst health crisis today (Italy), or the country likely to see the highest death rate (Spain), or the country in the worst financial position (Greece)?

Every time the Europeans face any sort of question that bridges the monetary and the budgetary, the eurozone finance and prime ministers have to meet to hash out their disagreements in marathon negotiating sessions that take days (if not months). In times of calm this is a questionable system which often borders on the comical. In times of crisis it is really really really really stupid.

It shows in the outcomes. During the 2008 financial crisis the Americans did more mitigation in three weeks than the Europeans did in nine years. This time around, the Americans did more in 48 hours than they did during the entire financial crisis.

The funding America’s Small Business Administration made available to provide bridge financing for America’s small businesses is a case in point. On day one $50 billion was unleashed, with another $350 billion to be available by April 1. The EU has no such established facility. Individual European governments are scrambling to raise the necessary cash for their own small businesses. Weaker EU states are unlikely to be able to raise the requisite funds without raiding their already rickety banks. With quarantines in place, entire countries shut down. Add in Europe’s far less flexible labor market and a workforce which remains wedded to old-style set-location facilities means European firms have more need for bridge financing than American ones, yet even Europe’s capacity to provide that financing is far lower.

Europe today is just getting going with its Rube-Goldberg-like-decisionmaking machine, and this time around coronavirus quarantines prevent the European leadership from even meeting in person to hash out a plan. The only European leader with gravitas, German Chancellor Angela Merkel, is in isolation due to potential coronavirus exposure.

Which means “Europe” cannot be part of the mitigation process.

That leads us six places, none of which are good. First, European investors know all this and they aren’t flooding their money into European assets. Instead, it’s a massive flight to US dollar assets. Expect the USD to continue to rise throughout the crisis.

Second, an exception to that rule will only increase the light between the various European governments. Germany, unlike most of Europe, has steadily whittled away at its debt levels to the point that pre-crisis there was a shortage of high-quality, low-risk government debt on European financial markets. With Germany loosening the purse strings, investors will purchase German debt. It is the bulk of the rest of Europe that’s likely to be shunned. Deep, visceral splits between how the Germans and the bulk of the Union viewed finance existed before coronavirus.

Debates on the topic are already taking on the stench of desperation. On March 25 the leaders of France, Italy, Spain, Portugal, Ireland, Luxembourg, Slovenia, Belgium and Greece (aka countries who consistently find balancing their checkbooks difficult) called upon the EU to issue a joint debt instrument to deal with coronavirus. Germans are likely to have a different opinion.

Third, when the scale of the capital flight and budgeting shortfalls becomes apparent, when European governments realize the money they need to try to save their systems is leaving, they will take action. Expect strict European capital controls at all levels. (China of course already has capital controls. Expect them to intensify.)

Fourth, the controls won’t be nearly enough. Even if the Europeans could prevent capital from leaving, raising capital to fund emergency spending the old-fashioned way isn’t as quick or effective as the American method of simply flipping the switch on the printing press. Firms would fold in the thousands, and the damage will not be limited to the small players. To stave off the subsequent economic and cultural carnage, expect mass nationalizations throughout European economies. Unsurprisingly, the French are already discussing the mechanics of how to manage this. Peugeot, Renault and Airbus have already indicated they will fight the process (although they’d still love help with recapitalization and operating costs).

Fifth, this is likely the end of “European” manufacturing. The European manufacturing system, especially the German manufacturing system, is based on the free movement of goods, people and capital across borders. That simply isn’t possible in an environment of national quarantine, capital flight, capital controls and nationalizations. Post-crisis things will still be made in Germany and Bulgaria and Sweden and so on, but not all that much is likely to be the result of a multi-national European supply chain.

This is doubly problematic in the short term as most European countries lack even small pieces of the medical supply chain. While the US can retool and China can get back to work, many European states simply don’t have anything within their borders they can use.

The dream of Europe was that open borders would enable Europe to have economies of scale of the Chinese or American type. But these are still separate countries, and the utter inability of the EU to ride to the rescue leaves individual states more or less on their own at the worst possible time. Germany, for one, is a major exporter of medical equipment, and it has already barred exports of many coronavirus-related materials. Even to its EU partners. Many Europeans already resent Germans’ unwillingness to share their wealth. Imagine how refusal to share medical equipment will go over once the death toll gets seriously scary.

Sixth, this is the end of the European economic and social model, and it risks being the end of “Europe” as an entity.

Europe’s demographics make consumption-led growth impossible, even as coronavirus blocks export-led growth.

The Americans were backing away from the global security rubric that makes Europe’s export-led growth model possible before coronavirus, and the virus is only accelerating America’s turning-inward.

Europe lacks the institutional capacity to manage crisis response.

Europe lacks the financial capacity to cope with the crisis, much less apply the sort of financial fire-hose the Americans did almost reflexively.

Dealing with the virus’ spread has already forced the Europeans to abandon the free movement of people.

Dealing with their financial shortfalls will force them to abandon the free movement of capital.

Dealing with mass nationalizations and the loss of export markets will force them to abandon the free movement of goods.

That’s three of the four freedoms upon which modern Europe relies. The fourth freedom – movement of services – was largely something that only the UK cared about, and the Brits are gone.

There is one possible “solution” to these problems: drop the euro.

If the Maastricht Treaty were abrogated (or at least suspended) and national control over monetary policy reintroduced, individual European countries could then engage in unlimited quantitative easing, both to mitigate the current crisis and to help manage the subsequent damage and recovery. This would (obviously) hold (many) downsides, but if the goal is to have the necessary capital required to address the current crisis, this is the only path I see that still results in salvaging Europe’s current economic and social structure.

In theory, once coronavirus was in the rear-view mirror, Europe could go through the process of re-merging their currencies (perhaps this time without basket cases like Greece). Yes, I realize this would be monumentally messy, but we’re already in a world where economic and financial norms are in abeyance. Most of contemporary Europe’s “messes” require extensive multi-national negotiations. This “plan” has the advantage of countries doing things themselves.

Regardless of the path forward (or down) coronavirus is just the beginning of Europe’s problems. Demographics, economics, financials, supply chains, none of it works under coronavirus – and coronavirus is going to be with us until we either get a vaccine, herd immunity or mass serological testing, none of which is particularly likely to happen in 2020. Even then, it is far from clear that Europe as we know it can reconstitute in the world after coronavirus. And never forget that all Europe is not created equal. Germany is not France is not Italy is not Poland is not Sweden is not Portugal is not Romania.

An end to the concept of “European” being singular represents more than simply the return to the norm of European history, it removes one of the central pillars of the world we know. That cascading failure and the reordering to come will be a subject in subsequent installments in our Coronavirus Guides series.

And now the pitch: the Coronavirus Guides are our primer documents, intended not to finish the discussions of this or that topic, but to launch them. Contact us at Zeihan.com/consulting to inquire about rates and scheduling options for teleconferences, videoconferences and in-depth consulting calls.