This is the first in a series of newsletters addressing the state of the COVID-19 pandemic around the world. Other articles in the series coverthe United States, the Persian Gulf, East Asia, Europe, and the BRICS.

For the next few days, the team here at Zeihan on Geopolitics will be sharing a few snapshots of the pandemic from around the world. This is less a holistic assessment and instead us taking the temperature of some major countries so that readers have an idea of the pandemic’s future trajectory.

As with all things coronavirus, the first question is where to start. Most COVID-related data is, in a word, unreliable.

New hospitalizations data are wildly misreported. Useful new deaths data assume patients were tested for COVID at all, and comparing death rates from COVID across countries assumes a common quality of care. Any hospital-related or death-related data assumes that the health system wasn’t overwhelmed (and so suffered no breakdowns in data collection) as well as being very well funded and staffed (and so had the luxury of being able to test everyone). Considering how infectious COVID is and how many health personnel have died of it, those can be tall bars in places where the epidemic rages hot.

So for this exercise we are using the dataset that is most cross-comparable: new cases as a percentage of the overall population.

It isn’t a perfect measure. Many, many countries – the United States included – have wildly insufficient testing regimes. Different countries (and different states, and different cities, and different hospitals) use different criteria when determining who to test. Nor is there a best-practices policy for how to report. Just as importantly, upwards of half of all COVID cases are asymptomatic, and even those who develop symptoms are typically presymptomatic for two to five days before symptoms set in. Everyone should assume that all new case data underreports the reality.

Perhaps most importantly, national data like this tends to mute local outbreaks such as what struck New York City, dissolving the intense local data within a national whole that is far less dramatic. So don’t use this series of newsletters as justification for actions either cautious or rash. It is nothing more than this: our best understanding of countries’ broad trajectories.

The raw data comes from the COVID Tracking Project and the European Centre for Disease Prevention and Control. The Financial Times runs the data through their graphics creator. In our opinion, access to the FT’s COVID interface all by itself more than justifies the FT’s full subscription price (and yet its free!).

We’re going to begin with Latin America.

Geography shapes all countries and populations, and a deep study of map sets can help you know what to look for. Latin America’s tell has to do with the balance of tropics and elevation. Life in the tropics is rough: lack of winter insect kills enables diseases to run rampant, most grain-based crops cannot ripen in the high humidity, simply getting concrete or asphalt to set is an aggravating exercise. As a result, most of Latin America’s largest cities are not on the coast, but instead upland to escape the heat and humidity.

A few fun points of reference: The United States only has one post office above 10,000 feet. The bulk of Bolivia’s population lives in the Altiplano, a region whose low point is at 12,000 feet. America’s highest elevation metro, Denver, famously sits one mile up; over half the Mexican population lives on a plateau over 2000 feet higher. Colombia’s major cities perch on the flanks of mountains too high to live atop.

Since infrastructure connections are few and crowded and expensive to build and maintain, living up high is expensive. But there can be perks (beyond the view): When infrastructure is a limiting factor, populations must concentrate where the roads go. One result? Dense population footprints. That somewhat simplifies the process of providing government services, services such as health care. While that services concentration certainly hasn’t prevented COVID outbreaks in Latin America, we feel it has provided the region as a whole with (slightly) more reliable testing data than the developing world writ large. Unlike India or Indonesia or Nigeria whose COVID numbers are hilariously low (more on all three in future newsletters), we feel Latin America’s data only understates the number of cases by a factor of five or less.

But what is most obvious is that no Latin American country has the epidemic under control. Throughout the region case loads are only building, and with vanishingly few exceptions (fingers crossed for Costa Rica) the virus is now likely endemic and we do not expect to see meaningful drops in case numbers until such time as a vaccine is widely available.

For Americans, the country that matters most is of course Mexico. The two neighbors have a great deal in common.

Both are federal systems with relatively weak central governments. Most policy decisions which impact day-to-day life – like say, anti-COVID efforts – are made at the state and local level. For both countries this is both good and bad. Good in that both countries are sprawling laboratories for best health practices. Bad in that the lack of national action on coronavirus has enabled the bug to become established everywhere.

The two countries also share a certain demographic geography, characterized by cities which freckle huge swathes of lightly populated territory. That means that as the COVID pandemic stretches on, both have the opportunity to isolate localized outbreaks without needing to shut down either country as a whole. Americans and Mexicans went into the outbreak together, they are dealing with the outbreak in more or less the same way, and they will come out of it together. That hardly makes everything firelight and marshmallows, but it befits a pair of countries who are now each other’s greatest and most reliable political, cultural, economic and security partners.

To that end, our next webinar – scheduled for June 16 – will be on the status of the Mexican system, ranging from manufacturing supply chains to the local COVID epidemic to debt markets to economic and diplomatic relations with the United States. Sign up information can be found here:

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

The past few several weeks have been busy for the Europeans, easily generating more events of consequence than at any time since at least the 2007 financial crisis. There is no specific trigger event here that makes much sense without absorbing the context first, so I’m just going to do what I do and start at the beginning.

Germans aren’t normal.

I don’t mean that as a condemnation of their weather or dourness or food or their linguistic tendency to link a dozen or more words together into typographical nightmares, but instead that Germany’s peculiar geography has made the Germans somewhat…peculiar.

Germany’s geography is the best and worst of all worlds. Best in that it boasts four major and a dozen minor rivers as well as ample stretches of flat land to both ease internal transport and make for cheap development. Worst in that Germany’s most rugged terrain is in the country’s interior while its flattest lands are on its borders, making it easier (historically speaking) for most Germans to integrate with their (non-German) neighbors rather than their own co-ethnics.

Historically, this has made German lands among the most bloodsoaked in Europe, with the whole area being preyed upon over and over and over. The first “Germany” was Charlemagne’s, and it only lasted so long as the great monarch was alive. The Holy Roman Empire was a primarily German entity (occasionally referred to as the First Reich), but it wasn’t even remotely united, comprised as it was by sometimes over 1000 (often mutually warring) statelets.

It was only with the onset of industrialization in the 1800s that Germans were able to use rail and electricity to overcome their internal geographic complexity and achieve unity. But unity doesn’t automatically translate into happy-fun-play-time. The second and third Reichs were Germany’s Imperial and Nazi incarnations. Those governments’ attempts to impose writs on the wider European neighborhood resulted in the most catastrophic wars humanity has ever experienced. For the following 45 years, Germany was the very definition of not united – split into two pieces to serve as mutually-opposing frontline states in the Cold War.

In the years since the Berlin Wall fell, the newly-united Germany – or Fourth Reich if you prefer – has been taking a wonderous vacation from history. It doesn’t need to fight to remain unified; America’s imposition of a global Order makes that unnecessary. It doesn’t need to protect its borders; American-dominated NATO takes care of security issues. It doesn’t need to fight for access to either raw materials or consumer markets. The Americans’ global structure has enabled the rise of the European Union within Europe, and has allowed German firms access to a worldful of consumption. All Germany needs to do to be Germany today is…be. And so the Germany of today is united, free and at peace…without the Germans needing to do a damn thing.

For those of you who would like Germany to exercise more decisionmaking power and take security matters into its own hands, I refer you to literally any book on European history between 1848 and 1945 to highlight why that might not be the fabulous idea you assume it to be.

Anywho, there are now three intersecting problems that all independently threaten Germany’s blissful existence.

First, the Americans are done holding up the collective civilizational ceiling of the world. The United States created the global Order to fight the Cold War, and that war ended when the Berlin Wall fell. The Americans have been edging away from, well, everything, ever since. The day of final abandonment was always going to come, it is now here, and everyone who used to shelter under the American security umbrella or benefit from a globalized economy must figure out a new way forward. That applies to Germany as much as everyone else.

Second, the German economic model of mass exports is running out of road. Mass exports requires a large, highly-skilled workforce heavy with people in their late-40s through early-60s. Germany has had that for the past 15 years, but those skilled workers collectively are crossing the retirement threshold this decade. With no replacement generation coming up through the ranks, Germany can neither consume what it produces today, nor maintain its current production for much longer. That eliminates both the basis of the German economy and the German tax base. Something new, something radical, something that utilizes resources beyond Germany, is required.

Third, the EU – the only meaningful piece of the Order the Americans do not directly control and so the only possible anchor the Germans have keeping them in a safe, peaceful, united Europe – is in mortal danger. In part it is because much of Europe faces the same security and export dependence upon the Americans as the Germans do. But there’s another problem.

Geography.

Northern Europe is flat and well-rivered and so countries there can achieve efficiencies and economies of scale. Southern Europe is rugged and lacks rivers and so cannot. Exceptions abound in a continent as varied as Europe, but the bottom line is that Southern Europe will never be able to compete with Northern Europe economically, just as Northern Europe cannot hope to compete with Southern Europe when it comes to sun, fun, food and flair. (France has a foot in both worlds which is part of what makes the French…well…French.) Anywho, the bottom line is that there is no European Union without both parts of Europe, so the question becomes how to keep it all stitched together without either the American-led Order or the ability to access markets from far beyond Europe?

There is no good answer. Even more problematic, what might prove a good answer for Ireland would be hilariously inappropriate for Croatia. What most everyone can agree on, however, is that Europe as a combined entity will be better able to get what it needs than the EU’s constituent members acting independently. And so Europe has been limping along since the 2007-2009 financial crisis, economically suppressed, strategically adrift, politically riven…but with no one (save the Brits) willing to pull the plug on the whole project.

In my new book, Disunited Nations, I’ve got a whole chapter on called “Superpower, Backfired” on the hows and whys Germany ended up in this situation and where it is likely to lead.

And then there’s the coronavirus.

Just as there are differences in European financial and economic structures on a country-by-country basis, so has the virus impacted EU members differently.

It comes down to vectors and weather. Most of the cases in Germany originated at a series of Alpine ski parties for 20-somethings. When the virus started to spread, it spread among the population most able to survive it. In addition, late-winter and early-spring in Germany isn’t exactly tourist season, so most elderly stayed locked up at home. Germany was able to address the virus outbreak relatively quickly and move on.

Not so in Italy. Patient zero went to a massive outdoor soccer game and became one of the first COVID superspreaders. Elderly Italians are also more likely to live in a multi-generational household than elderly Germans because…well… sun, fun, food and flair. It wasn’t long before the Italian health care system was overwhelmed.

Finances matter too of course. Germany has been whittling away at its national debt for twenty years, and so had plenty of dry powder to apply to the crisis without needing to ask anyone for help. Italy…hasn’t. When the crisis exploded upon the Italians they almost instantly ran out of cash and had to turn to the EU hat-in-hand for help.

The response was underwhelming. The Germans – backed up by the European Central Bank (ECB) chief – told the Italians that saving Italy wasn’t their job. As a point of comparison, across the Pond the Americans slapped together humanity’s largest-ever stimulus program in a matter of days.

It didn’t take long for German Chancellor Angela Merkel to realize that the situation was untenable. It wasn’t so much that Italy and others were facing fiscal collapse because of COVID (although they were), it was that Merkel knows full well that the road the EU is on means that Italy and others would inevitably face fiscal collapse. COVID just brought the end forward by a few years. The question Europe has been struggling with since 2007 – now that we are certain this is unsustainable, what do we do? – had moved from the hazy future to the here-and-now. And Merkel simply didn’t have an answer. If she had, she would have produced it. Years ago. And so the demurring and dithering continued.

Ironically, it took events within Germany itself to force the issue. On May 5 the German Constitutional Court ruled that methods the ECB were using to keep some of Europe’s weaker states on life support were unconstitutional. Specifically, the ECB can only purchase government debt if it does so proportionally to the size of all eurozone economies. Since the Germans have been paying their debt down, there wasn’t much German debt left to buy. And since the Italians were in a COVID pickle, the Italians needed to issue more debt. The ECB did the logical thing and put its resources where they were needed. The German court ruled that the ECB’s logic violated European law in general and the German constitution in specific, and that the German government must cease all cooperation on the issue within 90 days.

Running the European Central Bank without the participation of Europe’s largest economy would open up a hilariously huge barrel of worm-ridden monkeys, taking us down paths so convoluted and impractical as to be positively Venezuelan. But those monkeys and paths all take us to the same place: no European bond market, no European currency, and – very likely – no EU.

A world without America. A Europe without the EU. Germany left to look after its economic and security issues on its own, likely in competition with its current EU partners. That is nothing less than Merkel’s worst-case scenario, and so she did the only thing she felt she could:

On May 20 in a joint presser with French President Emmanuel Macron, Merkel proposed the EU’s first mutualized debt. For those of you not in finance, that’s a fancy way of saying that not only will Germany co-sign for some Italian borrowing, but that Berlin will agree up front to use the EU’s common budget to pay for some Italian spending. Simply put, Merkel committed Germany to paying for the ongoing existence of the EU in general and the EU’s weaker members in specific in the hopes of buying more time to find a better solution.

Many many details remain.

How big of a fund are we talking about? At present the combined floats of the Germans, French and the EU Commission total something around 1.5 trillion euro. (Right now that’s about $1.65 trillion US, so, you know, real money.) That’s roughly ten times the current total EU budget. That would probably cover the EU’s current needs this year, but only this year. And all the proposals to date are nothing more than one-offs designed to counter COVID impacts. This doesn’t actually help the EU survive in the long-run. For this to work and for the EU to function as a true superstate, the EU needs a full transfer union of at least these volumes annually.

Who would get the funds, and who would pay the funds back and how? At present the idea is to funnel everything through the European Commission, with funds being dispersed into (suddenly engorged) EU programs, while payback would come from the various member states who fund the Commission directly. Needless to say, that would be wildly inefficient and cumbersome, although it would wildly strengthen the EU’s administrative core and take Europe a few big steps down the road to full federalization on the American model.

Can this – institutionally – happen? It doesn’t look great. Big things like this normally require a treaty, and the EU has rarely managed negotiating and ratifying a treaty on anything less than a decade timescale. Moving forward without a treaty would still require unanimity, and several EU states have already voiced their vociferous opposite to the plan.

But, again, let me be clear here. Between the Americans’ withdrawal and Europe’s demographic implosion, the very existence of the European Union is at stake. This was always true. This was always inevitable. But COVID and the German court ruling makes the crisis imminent. In a Europe without either America or the EU, Germany must reorganize into a form that enables it to protect and further its own interests without outside support. This isn’t “simply” an existential crisis for the Germans. It is an existential crisis for all Europeans.

And historical annihilation tends to focus the mind.

So let’s take a brief look at the four hard-nos in this debate: Austria, the Netherlands, Denmark and Sweden.

The bulk of Austria’s population lives on the southern watershed of the Danube. The entirety of the Netherlands lies atop the delta of the Rhine. Those two rivers are core Germany population, industrial and transport zones. The Austrians and Dutch have zero geographic insulation from Germany.

Neither country may like the financial implications of where the debt-mutualization path leads, but both are deeply, painfully aware of precisely where European collapse leads: a Germany forced or induced to seek out German national interests to the detriment of its neighbors. Historically speaking, once the Germans get rolling, maintaining an independent Austria or Netherlands is pretty much impossible. The Austrians and the Dutch know this. Both can be armtwisted into accepting Merkel’s (costly) logic.

And that assumes Merkel doesn’t do her traditional thing. Unlike most leaders, Merkel tries to shun the spotlight and instead lead from behind. She allows her opponents to stake out bold positions, and then unobtrusively steps back from the shouting and quietly cobbles together a majority position that doesn’t include the troublemakers, leaving them with the option of joining the crowd or screaming into the void. She’s done this (repeatedly) to consolidate control of her political party in Germany. She’s done this (repeatedly) to defang troublesome governing coalition partners. She’s done this (repeatedly) to guide Europe through the financial crisis. It is highly likely that the Austrians and Dutch will be Merkel’s next void-screamers.

Denmark and Sweden are a different sort of challenge. Sweden doesn’t border Germany, while the bulk of the Danish population lives not in peninsular Denmark, but instead on the island of Zealand. Culturally, economically, and above all strategically both only have one foot in Continental Europe. In particular, both have historically been closer to the United Kingdom (and dare I say, the United States) on defense issues than to Germany. As such neither are even members of the eurozone. That makes the pair less likely to be cajoled into participation, but it also means there is another potential path.

Rather than run the funds and the debt through the EU budget, the funds could be kept aside as a purely eurozone project which could exempt any EU state that didn’t also use the European currency. (In addition to Denmark and Sweden, this list also includes a variety of Central European states such as Poland, Hungary and Romania.) It’d be messy organizationally, and arguably unnecessarily so, but the EU does tend to excel at spawning unnecessarily messy organizational structures.

Anywho, lots of details to work out. What Merkel and Macron are attempting on the fly is the first real step towards federalizing the European Union. Europe has a common currency (which not everyone is a part of) and a common foreign policy (which requires unanimity) and a common market (regulated by national governments), but until it has a common budget it is most certainly not a superstate and it is most certainly not pooling its national resources into a more powerful, more cohesive whole.

That more powerful, more cohesive whole is the only thing that matters if the EU is to persist through contorting geopolitical and demographic circumstances. There is no guarantee the current plan will be adopted, much less work, much less expand into something that would make the EU a true, durable power. But the fact remains that for the first time in years I have a faint glimmer of hope that this thing we call the European Union might, just might, survive.

On June 3 Melissa Taylor and Peter Zeihan will be hosting a video-conference on Manufacturing in a New Era. We’ll address the future of automotive, automation, reshoring, COVID’s shattering of supply chains, consumption shifts, as well as get you an update on the deepening trade war.

For those of you who don’t want to pop for the fee, we’ve recently completed a video on our projected shape of the COVID epidemic to come. You can watch it for free here.

Our June 3 manufacturing video-conference is only the first of a series which will include events focusing on Mexico, China, Energy and Agriculture. Scheduling and sign up information can be found here.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

Coronavirus is primarily a respiratory ailment primarily spread by exhaled droplets from coughs or simple breathing, which is why masks are so effective at preventing an infected individual from spreading it.

This obviously presents a few problems. Most people are completely asymptomatic for the first five days they harbor the virus. Any effort at an economic reopening must limit asymptomatic spreading, and the best way to do that is to maintain distance between individuals.

Which brings us to the graphic. It breaks down the American work force by distance. Any profession close to the top is one in which distancing at work is flat-out impossible. As one moves down the list, distancing becomes more and more built into the normal workflow.

The categories are fairly straightforward.

Green indicates medical service professionals. Obviously they have no choice but to be proximate to patients.

Orange are the folks who keep the food system flowing, which is about as essential as a worker can get. Not included are retail operations like bars and restaurants. Do we like them? Yes. But essential workers they are not.

Blue is where things get tricky. Not everyone who works in construction and infrastructure and power and transport may be “essential,” but there is no way the economy can get back to anything approaching normal without them. Without all of them. Moving forward, this group will become every bit as important as medical staff and food workers.

There are many pearls and ah-has in this information. (By the way, thanks to the folks at O*NET for maintaining the database! You can see the entire American workforce broken down by distancing needs here.) One of our chief takeaways is how traditional manufacturing jobs are not high up on the list. With very few exceptions (millwrights come to mind) most of those jobs are coded in the 60s and (well) below. That hardly means manufacturing workers are immune to COVID, but it does indicate that maintaining a degree of distancing is at least possible in a way that it just isn’t in a meatpacking plant or a hospital.

Which brings me to our upcoming video-conference series.

On June 3 Melissa Taylor and Peter Zeihan will be hosting a video-conference on Manufacturing in a New Era. We’ll address the future of automotive, automation, reshoring, COVID’s shattering of supply chains, consumption shifts, as well as get you an update on the deepening trade war.

For those of you who don’t want to pop for the fee, we’ve recently completed a video on our projected shape of the COVID epidemic to come. You can watch it for free here.

Our June 3 manufacturing video-conference is only the first of a series which will include events focusing on Mexico, China, Energy and Agriculture. Scheduling and sign up information can be found here.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

In the coming months, my team and I will be presenting on a wide range of topics that hit on the ways various industries and countries are adapting – or not – to the current crisis and what we can expect next.

The set fee for the event is $750. This will include access to the recorded videoconference, a Q&A with the audience at the end of the presentation as well as a copy of the PDF.

We look forward to seeing you there. Please use the links below to register:

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

Today’s U.S. coronavirus case update is full of good, and bad, news.

First the good. American testing capacity continues to increase, having reached a sustainable level in excess of 300,000 per day. Having being stuck below 200,000 until very recently, it is good to see the United States finally breaking through several bottlenecks.

However, this needs to be kept in perspective. Portugal, one of the EU’s financial bailout cases, has been consistently testing at this level in per capita terms for weeks now. Portugal isn’t the outlier here. That’s the United States, which is in only now reaching a reasonable testing level for being early in the epidemic.

The most important word in that sentence is “early”.

The United States has not crushed its case load in the way the Koreans, Taiwanese, Singaporeans, Chinese, Irish, Australians or Germans have. There are two reasons for this.

First, the American lockdown was not nearly as stringent as most other countries. Most other countries prevented infected individuals from returning home where they might infect their family members. Such family-to-family transmissions in China were responsible for 80% of infections.

Second, the United States entered the epidemic later than other countries, so it enacted lockdowns later and so saw its case loads drop later. Belgium and Italy and France and Spain – the four hardest-hit European states – all entered the epidemic earlier than the United States, and yet the United States is loosening its lockdown earlier than the Europeans.

That means America’s “second wave” of infections will be nothing of the sort, because the “first wave” was never crushed down. The “first wave” will simply have been a step up in caseloads. America’s lockdown only reduced active cases by about one-quarter instead of the 85%+ necessary to truly crush the virus, and so the “second wave” will now begin from an already-elevated case load.

This removes the United States from the list of countries including China and Korea and Germany which have largely removed the virus from their populations, and instead shifts it to a list of countries including Brazil and India and Nigeria where coronavirus is now endemic.

And that changes the path of the pandemic and its impacts on a global scale.

On May 19 I’ll be doing a once around the world, laying out where we stand in the current crisis. Which countries are suffering most critically? Which are pulling ahead? What the shape of the pandemic will be in the weeks and months to come? What will the world look like once coronavirus is in our collective rear-view mirror? As with all the videoconferences, attendees will have the opportunity to submit questions during the event.

While most of these events are for a set fee, the May 19 event will be free of charge. We’ve managed to expand our technical capacity and so still have lots of seats. And should those fill up as well, fear not! We’ll be recording the entire videoconference and posting it upon completion. First release will be via this newsletter list which you can join on the newsletter page.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

So, good news, we’ve surmounted some technical difficulties and have been able to substantially expand our seats at the upcoming May 19 videoconference. It will be a once-around-the world examination of where we stand in and what to expect from the ongoing coronavirus pandemic. You can register at the link at the bottom of this newsletter:

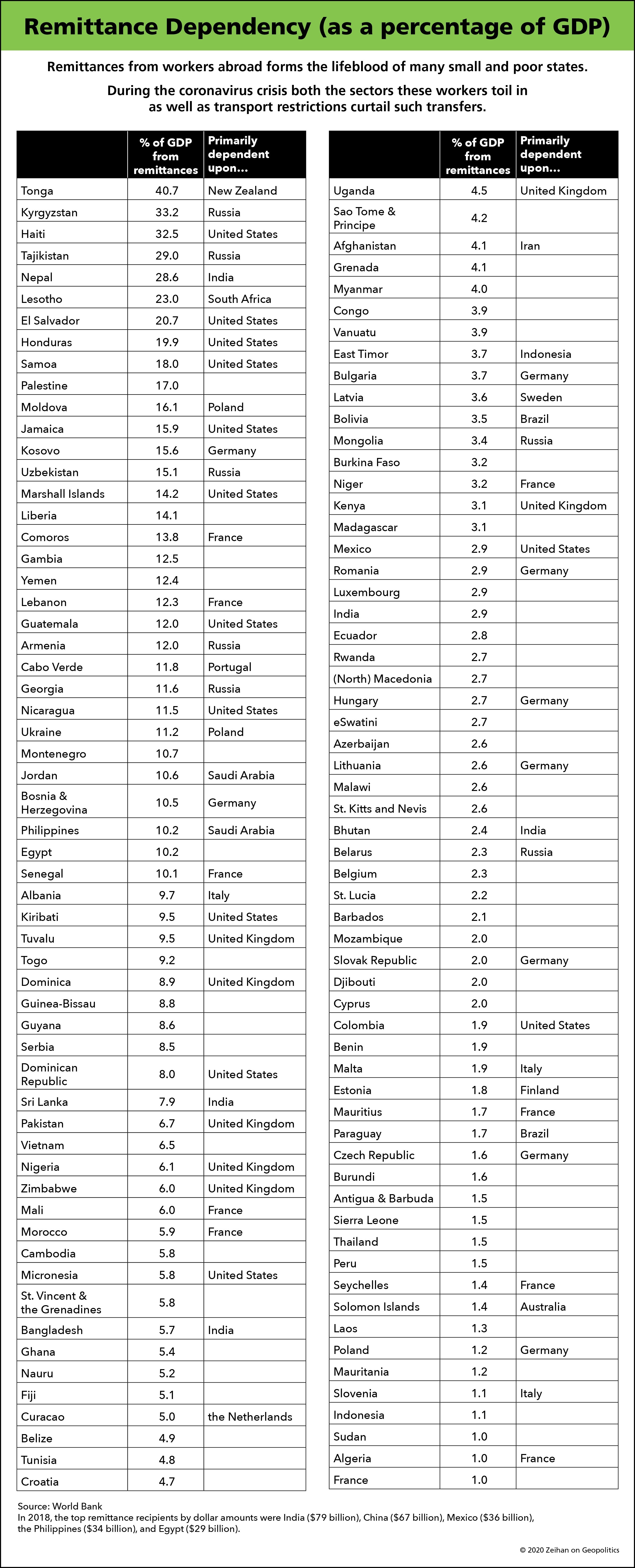

Part and parcel of the coronavirus epidemic is a general breakdown of international connections of all types. This impacts finance and manufacturing and transport and industrial commodities and on and on and on.

One “sector” that is often overlooked is migrant labor. Migrants do more than mow lawns and clean houses, they harvest crops and process meats and work in factories and build roads and homes. Some “migrants” even wear suits and work on Wall Street. They are a fact of life in every advanced – and many developing – economies.

During coronavirus lockdowns, their lives – like everyone else’s – are on hold. What makes migrants different from native workers, however, is that a big proportion of their income doesn’t stay with them. It is sent abroad where it often comprises the most important financial stream for their families back home. No income, no remittances. No remittances, and anyone the migrants support slips into poverty. While there are loads of exceptions (a Luxembourger working in the London financial district could be a “migrant”), as a rule the areas migrants come from are among the poorest in the world.

Somewhat ironically, and more than a bit tragically, a collapse in remittances tends to generate more migrants. After all, the alternative is to shelter in place in destitution.

On May 19 I’ll be doing a once around the world, laying out where we stand in the current crisis. Which countries are suffering most critically? Which are pulling ahead? What the shape of the pandemic will be in the weeks and months to come? What will the world look like once coronavirus is in our collective rear-view mirror? As with all the videoconferences, attendees will have the opportunity to submit questions during the event.

While most of these events are for a set fee, the May 19 event will be free of charge. We’ve managed to expand our technical capacity and so still have lots of seats. And should those fill up as well, fear not! We’ll be recording the entire videoconference and posting it upon completion. First release will be via this newsletter list which you can join on the newsletter page.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

The short version is that China’s spasming belligerency is a sign not of confidence and strength, but instead insecurity and weakness. It is an exceedingly appropriate response to the pickle the Chinese find themselves in.

Some of these problems arose because of coronavirus, of course. Chinese trade has collapsed from both the supply and demand sides. In the first quarter of 2020 China experienced its first recession since the reinvention of the Chinese economy under Deng Xiaoping in 1979. Blame for this recession can be fully (and accurately) laid at the feet of China’s coronavirus epidemic. But in Q2 China’s recession is certain to continue because the virus’ spread worldwide means China’s export-led economy doesn’t have anyone to export to.

Nor are China’s recent economic problems limited to coronavirus. One of the first things someone living in a rapidly industrializing economy does once their standard of living increases is purchase a car, but car purchases in China started turning negative nearly two years before coronavirus reared its head.

Why the collapse even in what “should” be happening with the economy? It really comes down to China’s financial model. In the United States (and to a lesser degree, in most of the advanced world) money is an economic good. Something that has value in and of itself, and so it should be applied with a degree of forethought for how efficiently it can be mobilized. This is why banks require collateral and/or business plans before they’ll fund loans.

That’s totally not how it works in China. In China, money – capital, to be more technical – is considered a political good, and it only has value if it can be used to achieve political goals. Common concepts in the advanced world such as rates of return or profit margins simply don’t exist in China, especially for the state owned enterprises (of which there are many) and other favored corporate giants that act as pillars of the economy. Does this generate growth? Sure. Explosive growth? Absolutely. Provide anyone with a bottomless supply of zero (or even subzero) percent loans and of course they’ll be able to employ scads of people and produce tsunamis of products and wash away any and all competition.

This is why China’s economy didn’t slow despite sky-high commodity prices in the 2000s – bottomless lending means Chinese businesses are not price sensitive. This is why Chinese exporters were able to out-compete firms the world over in manufactured goods – bottomless lending enabled them to subsidize their sales. This is why Chinese firms have been able to take over entire industries such as cement and steel fabrication – bottomless lending means the Chinese don’t care about the costs of the inputs or the market conditions for the outputs. This is why the One Belt One Road program has been so far reaching – bottomless lending means the Chinese produce without regard for market, and so don’t get tweaky about dumping product globally, even in locales no one has ever felt the need to build road or rail links to. (I mean, come on, a rail line through a bunch of poor, nearly-marketless post-Soviet ‘Stans’ to dust-poor, absolutely-marketless Afghanistan? Seriously, what does the winner get?)

Investment decisions not driven by the concept of returns tend to add up. Conservatively, corporate debt in China is about 150% of GDP. That doesn’t count federal government debt, or provincial government debt, or local government debt. Nor does it involve the bond market, or non-standard borrowing such as LendingTree-like person-to-person programs, or shadow financing designed to evade even China’s hyper-lax financial regulatory authorities. It doesn’t even include US dollar-denominated debt that cropped up in those rare moments when Beijing took a few baby steps to address the debt issue and so firms sought funds from outside of China. With that sort of attitude towards capital, it shouldn’t come as much of a surprise that China’s stock markets are in essence gambling dens utterly disconnected from issues of supply and labor and markets and logistics and cashflow (and legality). Simply put, in China, debt levels simply are not perceived as an issue.

Until suddenly, catastrophically, they are.

As every country or sector or firm that has followed a similar growth-over-productivity model has discovered, throwing more and more money into the system generates less and less activity. China has undoubtedly past that point where the model generates reasonable outcomes. China’s economy roughly quadrupled in size since 2000, but its debt load has increased by a factor of twenty-four. Since the 2007-2009 financial crisis China has added something like 100% of GDP of new debt, for increasingly middling results.

But more important than high debt levels is that eventually, inevitably, economic reality forces a correction. If this correction happens soon enough, it only takes down a small sliver of the system (think Enron’s death). If the inefficiencies are allowed to fester and expand, they might take down a whole sector (think America’s dot.com bust in 2000). If the distortions get too large, they can spread to other sectors and trigger a broader recession (think America’s 2007 subprime-initiated financial crisis). If they become systemic they can bring down not only the economy, but the political system (think Indonesia’s 1998 government collapse).

It is worse than it sounds. The CCP has long presented the Chinese citizenry with a strict social contract: the CCP enjoys an absolute political monopoly in exchange for providing steadily increasing standards of living. That means no elections. That means no unsanctioned protests. That means never establishing an independent legal or court system which might challenge CCP whim. It means firmly and permanently defining “China’s” interests as those of the CCP.

It makes the system firm, but so very, very brittle. And it means that the CCP fears – reasonably and accurately – that when the piper arrives it will mean the fall of the Party. Knowing full well both that the model is unsustainable and that China’s incarnation of the model is already past the use-by date, the CCP has chosen not to reform the Chinese economy for fear of being consumed by its own population.

The only short-term patch is to quadruple down on the long-term debt-debt-debt strategy that the CCP already knows no longer works, a strategy it has already followed more aggressively and for longer than any country previous, both in absolute and relative terms. The top tier of the Chinese Communist Party (CCP) – and most certainly Xi himself – realize that means China’s inevitable “correction” will be far worse than anything that has happened in any recessionary period anywhere in the world in the past several decades.

And of course that’s not all. China faces plenty of other of issues that range from the strategically hobbling to the truly system-killing.

China suffers from both poor soils and a drought-and-floodprone climatic geography. Its farmers can only keep China fed by applying five times the inputs of the global norm. This only works with, you guessed it, bottomless financing. So when China’s financial model inevitably fails, the country won’t simply suffer a subprime-style collapse in ever subsector simultaneously, it will face famine.

The archipelagic nature of the East Asian geography fences China off from the wider world, making economic access to it impossible without the very specific American-maintained global security environment of the past few decades.

China’s navy is largely designed around capturing a very specific bit of this First Island Chain, the island of Formosa (aka the country of Taiwan, aka the “rebellious Chinese province”). Problem is, China’s cruise-missile-heavy, short-range navy is utterly incapable of protecting China’s global supply chains, making China’s export-led economic model questionable at best.

Nor is home consumption an option. Pushing four decades of the One Child Policy means China has not only gutted its population growth and made the transition to a consumption-led economy technically impossible, but has now gone so far to bring the entire concept of “China” into question in the long-term.

Honestly, this – all of this – only scratches the surface. For the long and the short of just how weak and, to be blunt, doomed China is, I refer you my new book, Disunited Nations. Chapters 2 through 4 break down what makes for successful powers, global and otherwise…and how China fails on a historically unprecedented scale on each and every measure.

But on with the story of the day:

These are the broader strategic and economic dislocations and fractures embedded in the Chinese system. That explains the “why” as to why the Chinese leadership is terrified of their future. But what about the “why now?” Why has Xi chosen this moment to institute a political lockdown? After all, none of these problems are new.

There are two explanations. First, exports in specific:

The One Child Policy means that China can never be a true consumption-led system, but China is hardly the only country facing that particular problem. The bulk of the world – ranging from Canada to Germany to Brazil to Japan to Korea to Iran to Italy – have experienced catastrophic baby busts at various times during the past half century. In nearly all cases, populations are no longer young, with many not even being middle-aged. For most of the developed world, mass retirement and complete consumption collapses aren’t simply inevitable, they’ll arrive within the next 48 months.

And that was before coronavirus gutted consumption on a global scale, presenting every export-oriented system with an existential crisis. Which means China, a country whose political functioning and social stability is predicated upon export-led growth, needs to find a new reason for the population to support the CCP’s very existence.

The second explanation for the “why now?” is the status of Chinese trade in general:

Remember way back when to the glossy time before coronavirus when the world was all tense about the Americans and Chinese launching off into a knock-down, drag-out trade war?

Back on January 15 everyone decided to take a breather. The Chinese committed to a rough doubling of imports of American products, plus efforts to tamp down rampant intellectual property theft and counterfeiting, in exchange for a mix of tariff suspensions and reductions. Announced with much fanfare, this “Phase I” deal was supposed to set the stage for a subsequent, far larger “Phase II” deal in which the Americans planned to convince the Chinese to fundamentally rework their regulatory, finance, legal and subsidy structures.

These are all things the Chinese never had any intention of carrying out. All the concessions the Americans imagined are wound up in China’s debt-binge model. Granting them would unleash such massive economic, financial and political instability that the survival of the CCP itself would be called into question.

Any deal between any American administration and Beijing is only possible if the American administration first forces the issue. Pre-Trump, the last American administration to so force the issue was the W Bush administration at the height of the EP3 spy plane incident in mid-2001. Despite his faults, Donald Trump deserves credit for being the first president in the years since to expend political capital to compel the Chinese to the table.

But there’s more to a deal than its negotiation. There is also enforcement. In the utter absence of rule of law, enforcement requires even, unrelenting pressure akin to what the Americans did to the Soviets with Cold War era nuclear disarmament policy. No US administration has ever had the sort of bandwidth required to police a trade deal with a large, non-market economy. There are simply too many constantly moving pieces. The current American administration is particularly ill-suited to the task. The Trump administration’s tendency to tweet out a big announcement and then move on to the next shiny object means the Chinese discarded their “commitments” with confidence on the day they were made.

Which means the Sino-American trade relationship was always going to collapse, and the United States and China were always going to fall into acrimony. Coronavirus did the world a favor (or disfavor based upon where you stand) in delaying the degradation. In February and March the Chinese were under COVID’s heel and it was perfectly reasonable to give Beijing extra time. In April it was the Americans’ turn to be distracted.

Now, four months later, with the Americans emerging from their first coronavirus wave and edging back towards something that might at least rhyme with a shadow of normal, the bilateral relationship is coming back into focus – and it is obvious the Chinese deliberately and systematically lied to Trump. Such deception was pretty much baked in from the get-go. In part it is because the CCP has never been what I’d call an honest negotiating partner. In part it is because the CCP honestly doesn’t think the Chinese system can be reformed, particularly on issues such as rule of law. In part it is because the CCP honestly doesn’t think it could survive what the Americans want it to attempt. But in the current environment it all ends at the same place: I think we can all recall an example or three of how Trump responds when he feels personally aggrieved.

Which brings us to perhaps China’s most immediate problem. Nothing about the Chinese system – its political unity, its relative immunity from foreign threats, its ability import energy from a continent away, its ability to tap global markets to supply it with raw materials and markets to dump its products in, its ability to access the world beyond the First Island Chain – is possible without the global Order. And the global Order is not possible without America. No other country – no other coalition of countries – has the naval power to guarantee commercial shipments on the high seas. No commercial shipments, no trade. No trade, no export-led economies. No export-led economies…no China.

It isn’t so much that the Americans have always had the ability to destroy China in a day (although they have), but instead that it is only the Americans that could create the economic and strategic environment that has enabled China to survive as long as it has. Whether or not the proximate cause for the Chinese collapse is homegrown or imported from Washington is largely irrelevant to the uncaring winds of history, the point is that Xi believes the day is almost here.

Global consumption patterns have turned. China’s trade relations have turned. America’s politics have turned. And now, with the American-Chinese breach galloping into full view, Xi feels he has little choice but to prepare for the day everyone in the top ranks of the CCP always knew was coming: The day that China’s entire economic structure and strategic position crumbles. A full political lockdown is the only possible survival mechanism. So the “solution” is as dramatic as it is impactful:

Spawn so much international outcry that China experiences a nationalist reaction against everyone who is angry at China. Convince the Chinese population that nationalism is a suitable substitute for economic growth and security. And then use that nationalism to combat the inevitable domestic political firestorm when China doesn’t simply tank, but implodes.

With the world under COVID-related lockdowns, I’m pretty much as home-bound as everyone else. That’s nudged me to launch video conferences for interested parties on topics ranging from food safety to energy markets to the nature of the epidemic in the developing world.

On May 19 I’ll be doing a once around the world, laying out where we stand in the current crisis. Which countries are suffering most critically? Which are pulling ahead? What the shape of the pandemic will be in the weeks and months to come? What will the world look like once coronavirus is in our collective rear-view mirror? As with all the videoconferences, attendees will have the opportunity to submit questions during the event.

While most of these events are for a set fee, the May 19 event will be free of charge…which means it booked solid in less than a day. Fear not! We’ll be recording and posting it upon completion. First release will be via this newsletter list. If this was forwarded to you and you’d like to sign up yourself, you may do so here.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

The propaganda out of China of late has been…notable. Beijing has accused the French of using their nursing homes as death camps, has blamed Italy for being the source of the coronavirus (at the very peak of Italian deaths), has charged the US Army with bringing the virus to China in the first place, has thrown a “fact sheet” of truly disbelievable disinformation at the fact-oriented Germans, and turned the country’s ambassadorial core into cut-rate tabloid distributors – all while leaning on anyone and everyone from the United Nations to the World Health Organization to the European Union to regional legislative bodies to alternatively suppress and delete any information or analysis that does anything but laud China, as well as push them to take public stances that slobberingly praise China.

In doing so the Chinese have seemingly deliberately wrecked their relations with the Americans, French, Italians, Germans, Czechs, South Africans, Kazakhs and Nigerians, just to name a few. (The Swedes had all but ended their diplomatic relationship with China – having come to the public conclusion that the Chinese government was a pack of genocidal, power-mad, information-suppressing, exploitive, ultranationalists – before COVID.)

Nor are these disturbing shifts limited to the realm of foreign disinformation. Propaganda at home is boiling in a new direction as well. Overt, blatant racism is the core of the new program, with the government expressly blaming foreigners of all stripes for coronavirus in specific and China’s ills in general. Everything from restaurants to buses to gyms are banning foreigners. As a rule the government edicts are color-blind, but there are plenty of stories out there of this or that municipality or establishment singling out this or that nationality or skin color for…special consideration.

And the invective will get more offensive and self-destructive and seemingly stupid. China’s propaganda offensive April was done by the professionals – the folks at the head of the Ministry of Truth-, er, Foreign Affairs. All the lies and everything that demeaned and insulted countries in the grips of the coronavirus was expressly deliberate and sanctioned from the top, with the ambassadorial core directed to follow suit. (For those of you who like names, watch spokesman Zhao Lijian, a man who enjoys Chairman Xi’s personal sponsorship).

But we aren’t in April any longer, and China’s propaganda effort has become more diffuse, adopting more of a mob mentality. Now the entire governing apparatus has been unleashed, including agencies and bureaus down to the local level who normally have nothing to do with public relations, much less official propaganda. There is no longer a cohesive storytelling effort a la the Soviet style of propaganda. It is as if the Chinese equivalent of the MAGA crowd and the Bernie Bros are suddenly part of the propaganda effort, working alongside – or at least in parallel to – the Voice of America and the State Department.

The April propaganda was sophomoric and moronic, particularly at influencing foreign audiences or achieving some sort of strategic goal. In May it has already degraded into the realm of the infantile. My personal favorite was when an apparatchik made a lovely post stating “We condemn the fatso to death” with the “fatso” in question being US Secretary of State Mike Pompeo. Considering the ultrafine mesh the Chinese internal censorship dragnet has been using of late, that particular post’s ongoing longevity is a testament to just how holistic the CCP’s effort has become.

In the past few weeks the Chinese have deliberately destroyed three decades of efforts to build up soft power. I have never seen this sort of influence collapse, much less on a global scale. Even the Soviet fall saw Moscow retain influence throughout Latin America, Africa and the Middle East…and then the Soviet Union collapsed. The Trump administration just lost their Olympic gold in Gravitas Destruction to the Xi administration, and not by a small margin.

So…what the hell?

The Party may be descending into narcissistic ideology, and the Han Chinese may have always had a superiority complex based on a superiority complex, and we all may be a bit aghast at both the new tone and substance of Beijing’s foreign policy, and CCP is too paranoid, controlling, arrogant and bunkered to pretend to lead anything on a regional – much less global – scale, but I think we can all accept that the Party is not run by a bunch of morons.

The explanation is unfortunately very simple: the Chinese leadership is well aware that soft power isn’t what is going to solve the problem they see. There’s some guidance as to the CCP’s thinking in how the propaganda effort is being explained within China, and it doesn’t bode well for the future.

Semi-officially, the CCP called the April (official) effort Wolf Warrior diplomacy, in reference to a recent (and wildly popular) Chinese movie series about ethically pure Chinese soldiers who purge the world of evil American mercenaries. The closest equivalent I can think of would be like calling an American propaganda effort Starship Troopers diplomacy. (Yeah, it is as stupid as it sounds.)

The (more disperse) May effort, in contrast, is being referred to as a Yihetuan Movement mindset. It is a reference to a particularly chaotic period at the turn of the 19th to the 20th centuries when a particularly violent strain of ultranationalism erupted in response to foreign actions within China. Most non-Chinese readers probably don’t recognize the Yihetuan Movement reference, but they probably do recall how it was labelled in the West: the Boxer Rebellion. More on that in a minute.

This new propaganda program isn’t about Xi attempting to convince the wider world of China’s greatness or rightness. This isn’t about the United States or Europe or Africa, and certainly not about global domination. Instead it is about intentionally saying things so far beyond the pale that there’s a global anti-Chinese backlash. The backlash itself isn’t the goal, but instead a means to an end. Xi is attempting to use a global anti-Chinese backlash to enflame anti-foreigner nationalist activity within China. Put simply, Xi is trying to get the world pissed off at China so that China becomes pissed off at the world.

Xi feel he needs to hyperstimulate and mobilize a large enough proportion of the population so that they can assist the state security services in containing, demoralizing, cowing – and if necessary, beating, killing and disappearing – those who do not buy in.

Think this seems a bit…extreme? Brush up on your 20th century Chinese history, particularly in the context of how the CCP is explaining its propaganda effort to the Chinese citizenry.

Google the Great Leap Forward to review just how deliberately brutal the Chinese government can be to their own people, and just how good the Chinese government can be at motivating its own citizens to persecute one another.

Check out the Cultural Revolution to see how mobilizing portions of the population to repress the rest of the population makes the East German Stasi look like New Zealand socialists.

Review the Tiananmen Square massacre to remind yourself of how far the CCP will go even in “modern” times when it faces a threat to its power.

Look up the Boxer Rebellion to see how such processes result in the state-sponsored lynching and murder of Christians and foreigners. (Btw, if you are a manufacturer or investor and you still have personnel in China, now would be a glorious time to get them the fuck out).

The only part of this that is new for China is that this time they have industrial and digital technologies to help manage the population so that the sharp end of state power can be brought to bear more quickly.

This leaves only one question: Why…WHY would Chairman Xi feel this sort of extreme action is necessary?

Put simply, Xi fears the end of China is nigh.

And that, again, requires a completely new newsletter.

Stay tuned for Part III…

With the world under COVID-related lockdowns, I’m pretty much as home-bound as everyone else. That’s nudged me to launch video conferences for interested parties on topics ranging from food safety to energy markets to the nature of the epidemic in the developing world. While most of these events are for a set fee, my next video conference will be free of charge. Space, however, will be limited.

Join me May 19 for a once around the world of where we stand in the current crisis. Which countries are suffering most critically? Which are pulling ahead? What the shape of the pandemic will be in the weeks and months to come? What will the world look like once coronavirus is in our collective rear-view mirror? As with all the video conferences, attendees will have the opportunity to submit questions during the event.

Signups for the teleconference are first-come, first-served with attendance capped at 1000. After the event, we will make the video available, so watch this space.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

The past few weeks have been…eventful. I make my living anticipating and explaining and projecting change, with an unfortunate emphasis on destabilizing and disintegrative change. Pre-coronavirus the world was already hurtling through its most rapid breakdown in living memory; Coronavirus has accelerated…everything.

Times of extreme change are often painful, but for many they provide opportunity. Leaders often shine during times of extreme change. History tends to remember people who help their people and institutions navigate periods of disruption. Reagan’s speech at the Berlin Wall ended the Cold War. Yeltsin standing on a tank, defying the military put a bullet in the Soviet brain. Meir launching a worldwide assassination program made tiny Israel a global power. Churchill pledging to never surrender set the stage for the Nazi defeat. Ataturk defying Europe’s post-WWI carve-up plans ensured that, eventually, the Turks would return as a major power. In moments like these, a few countries pull away from the pack and reinvent themselves.

I haven’t seen any of that so far in the coronavirus crisis. Anywhere. Honestly, it is a little disappointing that no world leaders are rising to the challenge. While some leaders have dealt with the crisis competently, I haven’t seen any effort by any leader to harness the crisis to put their country on a more solid footing or to prepare for the post-COVID future. The lack of global leadership effort is simply mindboggling.

Let’s run through the list:

Emmanuel Macron has hitched his star to the idea that EU countries with solid budgets (that is, the countries less spendthrift than France) should shell out more money to help the poorer countries (that is, countries like France) get by. That certainly generates him some gravitas in Rome and Lisbon, but personifying the concept of asking for a hand-out isn’t what leadership looks like.

Germany’s Angela Merkel was supposed to be retired by now. Her chosen successor stepped back in early February, just before we all became obsessed with coronavirus. With her retirement plan in tatters, the Indispensable European is now once more unto the breach, dealing with intractable issues in her quiet, competent way. Unfortunately, she is constrained by her country’s savings-obsessed culture. No one in Germany wants to bail out Europe’s weaker members, particularly since Germany’s forward-looking, keep-your-powder-dry medical and financial approach has (so far) proven successful while Southern Europe’s spend-it-even-if-you-haven’t-got-it mindset has not. Honestly, Merkel looks like she’s just tired of it all. I feel exhausted just reading about her. (And frankly, she should be tired. She’s been shoveling Europe’s shit for over a decade.)

Even if everyone loved Brexit and how Prime Minister Boris Johnson has handled it, Johnson just now emerged from some quality time in a freaking COVID ward (just in time to bring his new baby home). The UK in general – and Johnson in particular – is in no shape to lead much of anything.

The orders to tamp down any discussion of coronavirus in Japan in order to maximize the chance of the 2020 Summer Olympics being derailed undoubtedly came from the top, making Prime Minister Shinzo Abe directly culpable in a spreading epidemic in the world’s oldest national demographic. Needless to say, few are looking to Tokyo for a how-to guide.

Canada’s Justin Trudeau has the look of a man who has been completely overtaken by events…because he has been. That’s less a judgment of his leadership or his team’s management skills, and more the crystallizing realization in Canada that there is no future for Canada unless it does everything of substance hand-in-glove with the United States. That includes trade policy and energy policy and China policy and…anti-COVID efforts. Trudeau has been (repeatedly) blindsided by whatever fresh spasms of oddity have erupted from the White House, and he simply has no option but to make the best of it. Pragmatic? Yes. Necessary? Certainly. But the liberal flame has most certainly gutted out.

Russia’s Vladimir Putin proudly proclaimed Russia had COVID “under control” just ten days before the Moscow mayor launched a lock down. There’s been broad spectrum public criticism by health care workers of the Russian government’s (mis)management of the epidemic, that has progressed to several doctors committing suicide by jumping out of buildings (a favorite technique of the Russian security services for disposing of troublesome personalities). This would be bad enough at any time, but Russia’s educational system collapse in the 1990s means Russia doesn’t have a particularly deep bench of health care staffers. COVID combined with the government’s response to the bad PR coming out of the health care sector is gutting what’s left of an already woefully inadequate health care infrastructure. Needless to say, while many countries want to manage the message, no one else is liquidating their precious health care workers to do so. (And incidentally, the Russian bot farms are hard at work spreading bat-shit crazy COVID-related conspiracy theories so please quit getting your COVID news from Facebook.)

Not to be left out, most of the world’s secondary powers have slightly wacky nationalist leaders who are proving…wackier with every passing day.

India’s Modi is working diligently to disenfranchise a large portion of his own population, and seems genuinely surprised when there is (violent) push back. Turkey’s Erdogan is gayly skipping his way down a neofascist path, setting the stage for (another) harsh, ethnic-based, wipe-out of a conflict with the Arabs to the south, the Europeans to the northwest, and the Russians to the northeast. Brazil’s Bolsonaro seems committed to ensuring the epidemic hits his country as hard as possible, in part by personally leading press-the-flesh rallies against COVID-containment and mitigation efforts. Mexico’s Andres Manuel Lopez Obrador is nearly as obtuse on the topic of the virus as Bolsonaro. Moreover, he has decided against providing much of any support to Mexican firms during the crisis, ensuring that Mexico’s recession will be longer and more difficult than it needed to be.

The number of leaders who have risen to the occasion is vanishingly small. Korea’s Moon Jae-in and Taiwan’s Tsai Ing-wen have done a phenomenal job of managing the COVID epidemic, but much of the credit must go to those countries’ intelligence and diplomatic corps who are arguably the most attuned to regional disruptions. After all, for them threat detection/assessment is a matter of day-to-day survival, and their hawklike watching of China is what provided their countries’ health services with the advance warning the situation necessitated.

Honestly, the only leader who has truly outperformed is Prime Minister Jacinda Ardern of New Zealand. But while Ms Ardern continues to impress, her country’s geographic isolation grants the Kiwis virus containment/limitation options denied the rest of humanity. There are a few lessons there for others, but only a few. Yet even with these three bright spots, no one outside of their respective countries is looking to Moon or Tsai or Ardern for leadership.

That holds true pretty much everywhere. With the possible exception of Angela Merkel, not many people have looked to any of these leaders to be authorities on regional issues, much less global ones…ever. Part and parcel of true global leadership is that there can really only be one. Since the Americans for the past 70 years have provided the security architecture and economic capacity for a global system to exist, it has fallen to the man in the White House to design the response, set the course, provide the resources and, to be blunt, lead. That’s triply true in the case of the meaningful international institutions which provide the sinew of global cooperation.

Those days are over.

Since his election, Donald Trump has functionally ended NATO, eliminating the single greatest security alliance in human history. Last year the Trump administration functionally destroyed the World Trade Organization, the only institution capable of empowering the multilateral trading system. Last month the Trump administration ended American funding for the World Health Organization. A flawed institution? Sure. But to abandon it during a pandemic was, in a word, questionable. The American alliance with South Korea – long one of America’s three most loyal allies – is likely to end this year at Trump’s behest. TeamTrump is even drawing up plans to pull intelligence assets out of the United Kingdom, America’s oldest, closest, and most capable ally, in protest over the Kingdom’s Huawei-linked telecoms policy.

It doesn’t really matter whether you think Trump’s actions are warranted or otherwise. The point is that the United States de facto controlled these institutions and alliances. By leaving or killing them while simultaneously failing to establish domestically-run alternatives, Trump has vastly reduced the ability of the United States to manipulate the world. That isn’t leadership. That is abdication.

Nor is it purely an international question. Domestically, Trump is a standout in that the longer he is in the White House, the less competent he appears to be at using the tools of domestic power.

I’m not talking here about Trump’s politics, policies, or even personality, but about his gob-smacking lack of managerial skills. Nearly three and a half years into his term, there are still hundreds of positions throughout the federal bureaucracy which remain unfilled, a disturbing number of which deal with issues of health. Headless bureaucracies are broadly useless except to carry out the last orders that they were given. It is with more than a touch of irony that I must note that despite all sound and fury to the contrary, Trump’s pathological unwillingness to engage with the federal bureaucracies has actually entrenched Obama’s regulatory disfunction rather than excised it.

Nor has much of what Trump has done trimmed those bureaucracies down to size. After all, reducing staff and mandates and budgetary outlays takes active leadership, and Trump is one singularly disinterested and disengaged leader. Since Trump hasn’t disbanded the agencies or programs, America has been landed with all the expenses of a sprawling bureaucracy, but few of the benefits.

Add in daily COVID briefings in which Trump seems pathologically committed to showcasing his furiously deliberate lack of knowledge, and Trump’s levels of respect at home and abroad are at the lowest of his presidency – and trending very firmly down. Imagine how weak he will look in a few months (weeks?) when the United States experiences its second coronavirus wave.

Absent from this list of not-necessarily-failed-but-certainly-not-successful leaders is, of course, China’s Chairman Xi Jinping. Understanding just how disastrously Xi has mismanaged the coronavirus crisis and just how much permanent, irrevocable damage his “leadership” is causing China requires an entirely independent newsletter.

Stay tuned for Part II…

With the world under COVID-related lockdowns, I’m pretty much as home-bound as everyone else. That’s nudged me to launch video conferences for interested parties on topics ranging from food safety to energy markets to the nature of the epidemic in the developing world. While most of these events are for a set fee, my next video conference will be free of charge. Space, however, will be limited.

Join me May 19 for a once around the world of where we stand in the current crisis. Which countries are suffering most critically? Which are pulling ahead? What the shape of the pandemic will be in the weeks and months to come? What will the world look like once coronavirus is in our collective rear-view mirror? As with all the video conferences, attendees will have the opportunity to submit questions during the event.

Newsletters from Zeihan on Geopolitics have always been and always will be free of charge. However, if you enjoy them or find them useful, please consider showing your appreciation via a donation to Feeding America. One of the biggest problems the United States faces at present is food dislocation: pre-COVID, nearly 40% of all foods were not consumed at home. Instead they were destined for places like restaurants and college dorms. Shifting the supply chain to grocery stores takes time and money, but people need food now. Some 23 million students used to be on school lunches, for example. That servicing has evaporated. Feeding America helps bridge the gap between America’s food supply (which remains robust) and its demand (which coronavirus has shifted faster than the supply chains can keep up).

A little goes a very long way. For a single dollar, FA can feed one person for three days.

In the past five weeks the United States has thrown $3 trillion in new government spending at coronavirus-related bailouts, relief and economic stimulus. In total the US has already spent more on coronavirus-related actions than the rest of the world combined, tripled. Strangest of all, not one dime of it is backed up by new government revenue streams; every bit is deficit spending.

Nor is the United States likely to overly suffer from the expansion of its debt burden. Of that $3 trillion in new spending, the Federal Reserve’s total purchases of US debt is “only” $1.3 trillion. The rest of the debt bulk has been absorbed by other investors, mostly foreign investors. Such is the scare globally that many are eager to get a zero rate of return on an American government asset rather than risk their money at home.